Sakura Research is LONG RAFFLES MEDICAL GROUP (SGX:BSL).

We think that the fair value of RMG shares should be greater than S$2.60.

THE RESEARCH EXPRESSES SOLELY OUR OPINIONS.

Viewing and/or use of Sakura Research materials is at your own risk.

Executive Summary

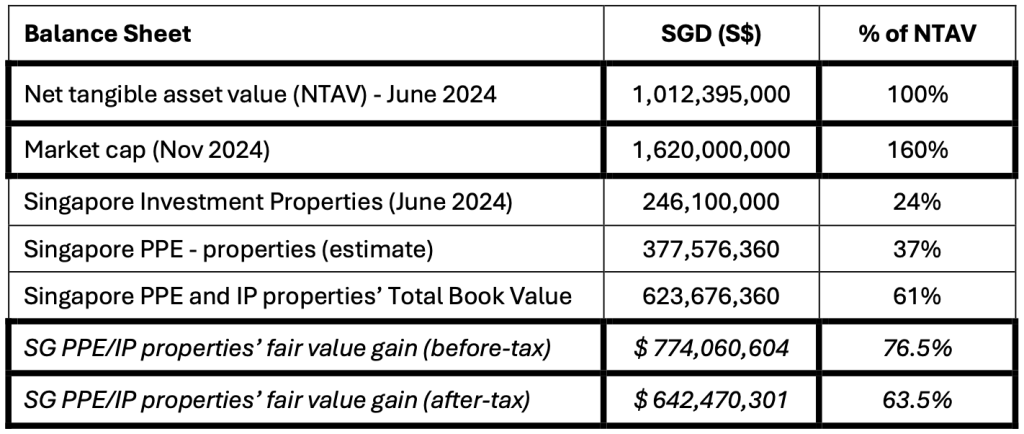

RMG’s June 2024 net tangible asset value of S$1.012b includes S$316m in cash; and approximately S$624m (61% of NTAV) in prime Singapore real estate assets: S$246m in investment properties, which generate rental income, and approximately S$377m in PPE properties.

RMG shares are currently trading at a 52-week low, with a market cap of S$1.6 billion, while the local stock benchmark (STI) is near its 52-week high. Aggressive share purchases by the Founder/Executive Director, increasing his ownership to more than 55%, have recently caught market’s attention, including ours. Our diligence has uncovered interesting facts regarding RMG’s Singapore properties.

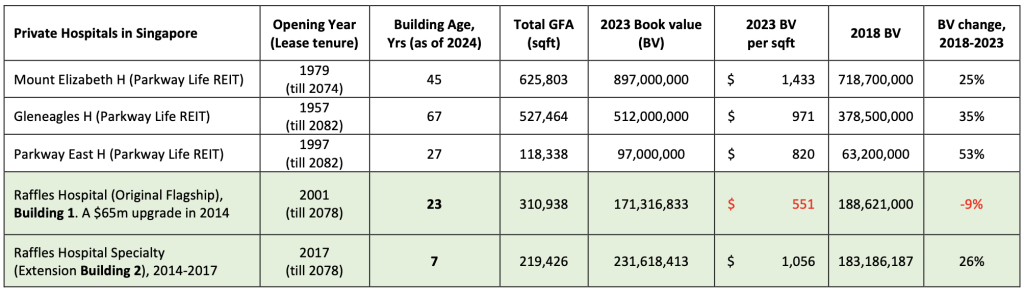

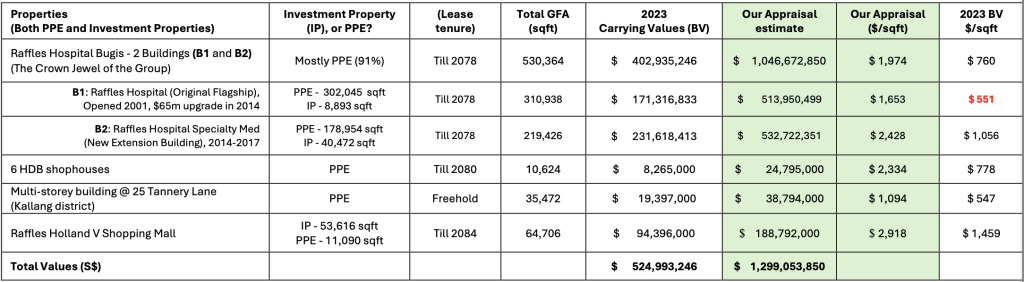

The Crown Jewel of the Group, Flagship Hospital at Bugis Downtown, consists of 2 buildings with total gross floor area of 530,000 sqft and has a carrying value of S$402m as of the end 2023. Peer comparison analysis, particularly with IHH Healthcare (operator of Mount Elizabeth, Gleneagles, and Parkway East hospitals) in Singapore, indicates that Raffles Hospital’s buildings are more than three times newer, built more recently with modern construction designs, and benefit from a strategic Downtown location. Additionally, Raffles Hospital boasts superior asset efficiency, with higher revenue yields. Furthermore, land and construction costs in Singapore have risen significantly since the 2010s. As a result, the carrying value of the Crown Jewel should be adjusted to reflect its market value, with an estimated fair value upgrade to S$1,046 million (i.e., S$1,974 per sqft, compared to the carrying value of S$760 per sqft as of the end of 2023).

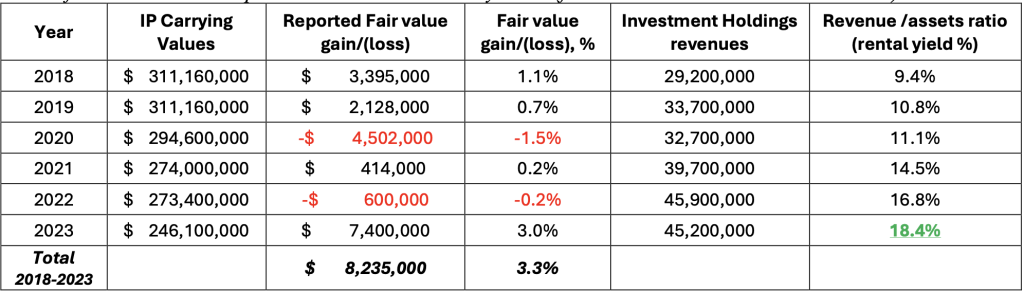

Investment Properties. From 2018 to 2023, the Group’s reported total fair value gains from investment properties has been around 3% net, while their generated revenues have risen by about 55% (from S$29.2m in 2018 to S$45.2 in 2023). As such, RMG’s investment properties rental yield (annual revenues divided by the carrying values) has been increasing steadily from 2018 to 2023, achieving an impressive 18.4% rental yield in 2023 vs. 9.4% in 2018. Meanwhile, the local hospital REIT (Parkway Life REIT) Singapore rental yields have averaged ~6% annually during the same period due to the REIT’s regular fair value gains of its properties. Again, the rental yield comparison implies that the Group’s investment properties carrying value is about 3x lower than a local peer, supporting our thesis of ridiculous under-appraisal of RMG’s Singapore investment properties.

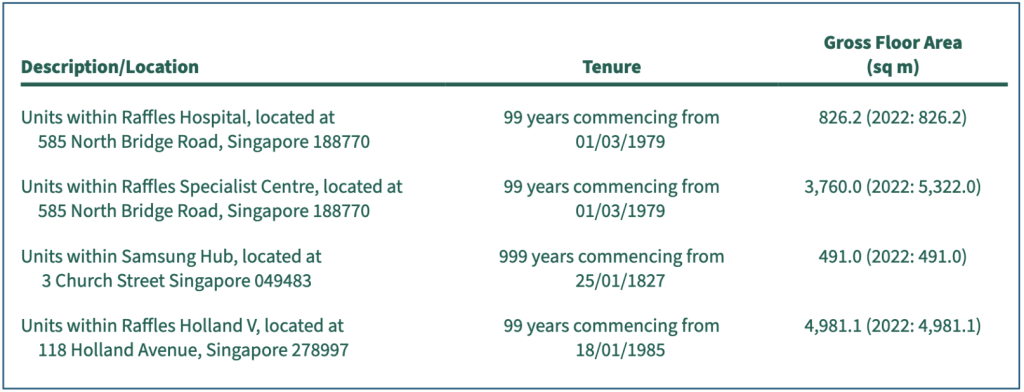

Raffles Holland V Shopping Mall (GFA of 64,706 sqft, with 83% of the asset used as an investment property by the Group) is currently valued at S$94 million on the balance sheet (at S$1,459 per sqft). However, we believe it’s fair market value is closer to S$188 million (at S$2,918 per sqft) due to its higher rental yield, strategic location, and excellent connectivity.

RMG also owns 6 HDB shophouses as part of PPE, with a total gross floor area of 987 sqm (10,624 sqft), and total carrying value of $8.265m as of end-2023, instead of our estimate of S$24.7m. During 2023, the Group sold one unit. The sale price was S$518,000, a 200% premium over the book value of S$174,000, again supporting our thesis of ridiculous under-appraisal of RMG’s SG properties.

Conclusion

Overall, our study shows that RMG’s Singapore properties are clearly and persistently under- appraised. We estimate a pre-tax fair value gain of approximately S$774 million for RMG’s Singapore properties (or S$642 million after-tax, reflecting a 63% premium over RMG’s net tangible asset value of S$1.012 billion) based on a mark-to-market analysis.

Curiously, RMG has changed its Singapore appraiser in 2021, from Jones Lang LaSalle (JLL) to Colliers International. Given the significant under-appraisal of prime Singapore real estate assets since 2018 compared to the local peers and RMG shares at 52wk lows, it is concerning that there has not been a single share buyback to benefit all shareholders since December 2023. However, the largest shareholder/Executive Chairman has been steadily increasing his stake in RMG.

Appraisers should properly value the company’s prime real estate assets by employing a local peer comparison approach, assessing revenue generation capacities, rental yields, and comparable market sales. Relying solely on Level-3 fair value assumptions and estimates, which have been in place well before COVID19, is no longer sufficient. A more accurate and market-reflective valuation is essential to ensure that all shareholders benefit from the true value of the company’s prime assets (not just the controlling shareholder/Executive Chairman Dr. Loo).

RAFFLES MEDICAL GROUP

RMG (the “Group”, or the “Firm”) is a beloved success story of “two young punk doctors who quit stable jobs to challenge norms in Singapore’s medical practice” – Dr. Loo Choon Yong and Dr. Alfred Loh. Today, the Group is a key private healthcare provider in Singapore with an amazing brand value and popularity. Its stock has lagged the wider market this year, dropping about 20% since the start of this year while the local Straits Times Index (STI) has risen about 15%.

It has come to market’s attention that the group’s Chairman and Co-founder, Dr. Loo, has been actively acquiring shares and increasing his stake to a record 55%.2 Upon further investigation into the company’s balance sheet, we have discovered true gems: the prime and relatively young, undervalued Singapore-based properties owned by RMG. These properties are poised for revaluation due to their more modern buildings, attractive locations, abnormally high rental yields and high revenue generation capacities compared to the local peers, amid the rising construction and land prices in Singapore.

I. Mark-to-Market: Justifications for Fair Value Gains – Raffles Hospital (The Crown Jewel)

The prime property is the flagship Raffles Hospital building, located in the downtown Bugis area. The building has a Gross Floor Area (GFA) of 310,938 sqft and opened in 2001. It was further renovated after 2014 with an investment of approximately S$65 million. Between 2014 and 2017, the Raffles Hospital Specialty (Building Extension) was added on newly acquired land (GFA of 219,426 sqft) at the same Bugis Downtown address. As a result, Raffles Hospital Downtown Bugis with total GFA of 530,363 sqft became the Crown Jewel of the Group. Most of the Bugis properties is used by the Group as property, plant, and equipment (PPE) for its hospital and healthcare services. The remaining 9.3% portion (GFA of 49,365 sqft) of the Raffles Hospital Bugis properties is classified as an Investment Property, generating rental income.

a) Appraisal Value Determination via Private Hospitals Peer Comparison

The firm’s local competitor, IHH Healthcare (SGX: Q0F), is a global healthcare services provider, and it is the largest shareholder of Parkway Life REIT. The Parkway REIT’s Singapore portfolio is 3 Singapore-based private hospitals (Mount Elizabeth Hospital, Gleneagles, and Parkway East) with a total carrying value of S$1.506B as of the end 2023 (about 30% fair value gains since 2018).3While Parkway Life REIT has consistently reported higher appraisal values for its much older Singapore hospitals (compared to the newer Raffles Hospital Bugis buildings), the Group has been decreasing its reported carrying values. For example, competitor Mount Elizabeth Hospital, which opened in 1979, shows a carrying value of $1,433 per square foot in 2023, while the Raffles Hospital Building 1, which opened in 2001, has a carrying value of only $551 per sqft as of the end 2023.

b) Modern Construction & Strategic Location

Raffles Hospital Downtown (310,938 sqft) was originally opened in 2001 using modern building technologies, followed by a redevelopment and renovation in 2014, which involved an investment of approximately S$65m. Additionally, an extension building with GFA of 219,426 sqft for specialty medicine was added between 2014 and 2017 at the same address, after the land was acquired in 2014.

The Bugis Raffles hospital’s building age, weighted by square footage, is significantly younger compared to other similar private hospitals in Singapore. For instance, compared to Mount Elizabeth Hospital (opened in 1979) and Gleneagles Hospital (opened in 1957), Raffles Hospital Bugis properties are 3.3 times younger based on a square footage-weighted average. The entire Raffles Hospital Downtown complex also benefits from an excellent location, just a 3-minute walk from Bugis MRT interchange, which connects the Green and Blue lines. This central location further enhances the property’s value, making it a prime asset in the heart of Singapore.

c) Superior Asset Efficiency & Revenue Yield of Raffles Hospital vs the local competitor

The Crown Jewel (Raffles Hospital Downtown Bugis) demonstrates a significantly higher revenue- to-asset yield ratio compared to its competitor, IHH Healthcare, in Singapore. In 2023, Raffles generated a revenue-to-assets yield of 92.1%, substantially higher than IHH’s 34.5%. This indicates that Raffles Hospital’s assets are being used more efficiently to generate revenues (cash flows), which further supports a higher property valuation compared to the local peer. As shown in the Table 2 below, Raffles Group’s ability to generate higher sales per unit of non-current assets in Singapore underscores the urgent need for the property’s reappraisal (Table 2).

d) Rising Construction, Material, and Land Costs in Singapore

The fair value estimate of the Crown Jewel (Raffles Hospital Downtown) should also be revised upwards to reflect the significant increase in construction, material, and land costs since 2014 in Singapore. In 2022, the Group recognized approximately S$10m impairment on its two hospitals in China, citing declining land and construction costs in China (Annual Report 2022, page 148). In the same vein, given the massive increase in land and construction costs in Singapore since the 2010s, the fair value of Raffles Hospital Downtown with a total GFA of 530,363 sqft should be marked up to market accordingly.

o Land: Market Approach – based on current market price per square meter.

o Buildings: Cost Approach – using the depreciated replacement cost method, adjusted for current market construction costs.

Based on the factors outlined above— local peer private hospital appraisal values, Raffles Hospital’s modern construction with newer buildings, strategic location, superior revenue generation efficiency, and the general rising construction and land costs in Singapore —our revised valuation for Raffles Hospital Downtown (the Crown Jewel of the Group) is S$1,046,672,850, which is significantly higher (at ~160% premium) than its carrying value of S$402,935,246 as of the end of 2023.

II. Rental yield comparison of the Group’s Investment Properties (IP) and a local competitor

The Group’s Investment Properties (with a carrying value of S$246.1m as of the end-2023), which have long been under-appraised, have demonstrated increasing investment holding revenues. Specifically, the annual rental income from the firm’s Investment Holdings has risen by approximately 54%, from S$29.2 million in 2018 to S$45.2 million in 2023. However, despite this growth in rental income, the firm has reported that the total fair value gain of its Investment Properties has increased by only 3.3% net over the same period (the sum of annual fair value gains and losses, from 2018 to 2023) (Table 3).

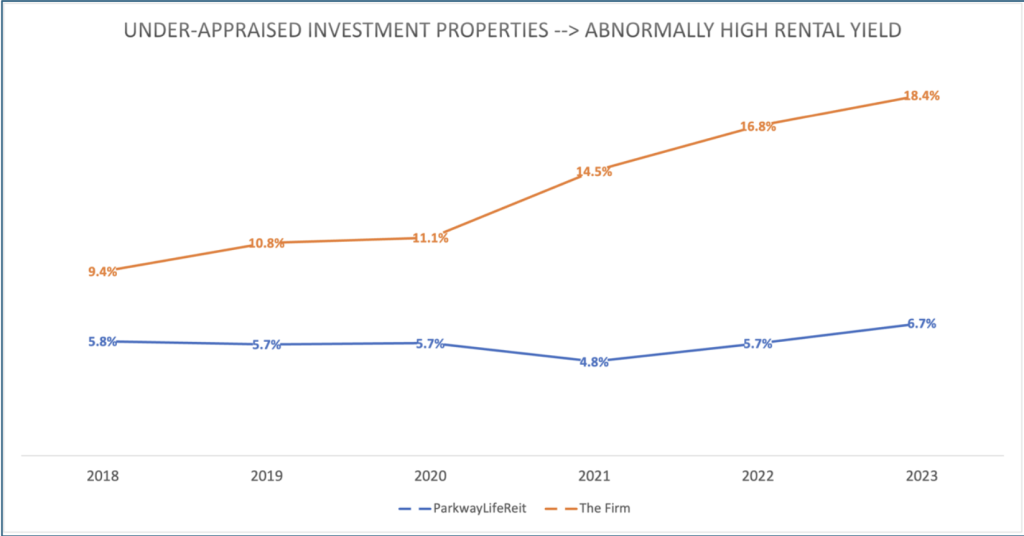

A comparison of annual rental yields between the firm’s Investment Properties and those of a local competitor, Parkway Life REIT, reveals a notable discrepancy. Parkway Life REIT’s properties in Singapore have an annual gross rental yield of around 5%–6%, while the firm’s Investment Properties have seen a sharp increase in rental yield, rising from 9.4% in 2018 to 18.4% in 2023 (Table 4).

This significant jump in yield further emphasizes the chronic under-appraisal of the fair value of the Group’s Investment Properties.

Given the empirical evidence of abnormally high rental yields (about 3 times higher than the local competitor), it is obvious that the carrying values of RMG’s Investment Properties should be adjusted to reflect their market values. A fair mark-to-market adjustment suggests that the carrying value of the firm’s Investment Properties should be increased by 200% (from S$246.1m in June-2024 to S$738m).

III. Mark-to-Market: Other Notable Singapore Real Estate Assets Ripe for Fair Value Gains

a) The Group also owns 6 HDB shophouses with a total gross floor area of 987 sqm (10,624 sqft), and total carrying value of $8.265m as of 2023. The Group’s reported carrying values have dropped 15% from $9.675m in 2017. However, the carrying values of these HDB shophouses should be revised upward to S$24.795m (200% premium over the carrying values of Dec-2023).

This point is proven by the Group’s recent sales transaction in 2023 (a unit with an area of 112 sqm). This property was carried at a book value of $174k at the end of 2022, while the Group received $518k consideration during the 2023 property sale, that is approximately 200% premium market price vs. its book value! (RMG Annual Report 2023, page 161).

b) Another significant RMG property is a large freehold building located at 25 Tannery Lane in the Kallang district, with GFA of 35,472 sqft. The Group has been gradually reducing the carrying value of this asset since 2018. However, the asset’s current market value is estimated at around $38 million, which is substantially higher than its book value of $19 million on the Group’s balance sheet.

c) Another key RMG asset is the Raffles Holland V Mall, with a Gross Floor Area (GFA) of 64,706 sqft. The property is primarily held as an investment to generate rental income, while a smaller portion (11,086 sqft) is used by the Group for its clinics under Property, Plant, and Equipment (PPE). Given its strong rental yield, prime location, and excellent connectivity, the fair market value of the mall is closer to S$188 million, equating to approximately S$2,918 per sqft.

CONCLUSION

In summary, we estimate that the Group’s Singapore property values should be marked to market with a total fair value gain of S$774 million. These are empirically proven by publicly-listed local peer’s private hospitals, the impressively high rental yields of the Group’s Investment properties (3x more than the peer), the higher revenue yield of the Group’s Singapore assets (3x more than the peer), and recent property sales by the Group with 200% premium over the carrying value.

The accounting statements are supposed to reflect economic reality. To address the raised mis-appraisal issues, it is imperative that the management & the BoD hire a competent independent appraisal firm—such as CBRE or KF, who have worked on Parkway Life REIT Singapore hospitals portfolio. This team should properly value the company’s prime real estate assets by employing a peer comparison approach, assessing revenue generation capacities, rental yields, and comparable market sales. Relying solely on rigid Level-3 fair value estimates, which have been in place well before COVID-19, is no longer sufficient. A more accurate and market-reflective valuation is essential to ensure that all shareholders benefit from the true value of RMG assets.

References

1) The Group’s Singapore exchange filings

https://www.sgx.com/securities/company- announcements?value=RAFFLES%20MEDICAL%20GROUP%20LTD&type=company&pa ge=1&pagesize=100

2) Parkway Life Real Estate Investment Trust annual reports https://plifereit.listedcompany.com/ar.html

3) The Group’s RMG annual reports

https://www.rafflesmedicalgroup.com/investor-relations/results-and-reports/annual- and-sustainability-reports/

4) IHH Healthcare annual reports

https://www.ihhhealthcare.com/investors/reports-presentation/reports-and-presentations

By viewing material on this website you agree to our Terms.

View and/or Use of Sakura Research materials is at your own risk.

THE RESEARCH REPORT EXPRESSES SOLELY OUR OPINIONS.

Opinions only.

SakuraResearch.com

medium.com/@SakuraResearch

Contact info {at} SakuraResearch {dot} com

https://x.com/sakuraresearch