Greater China Operations with Massive Accumulated Losses: Pursuit of Sustainable & Profitable Growth amid Succession Planning.

Sakura Research is LONG RAFFLES MEDICAL GROUP (SGX:BSL).

We think that the fair value of RMG shares should be greater than S$2.60.

TERMS APPLY.

OPINIONS ONLY.

EXECUTIVE SUMMARY

Since 2017, RMG has been making investments outside Singapore, primarily in Greater China, where it has built three newly constructed “greenfield” hospitals in Shanghai, Beijing, and Chongqing. China was viewed as a growing economy with a rising number of affluent consumers capable of affording RMG’s modern and premium medical services. However, after COVID-19, China’s appeal to foreign investors has dramatically diminished due to the endless series of negative developments: a property market collapse, weakened consumer demand, the “common prosperity” campaign, trade wars, an expat exodus, heightened local competition, and regulatory changes.

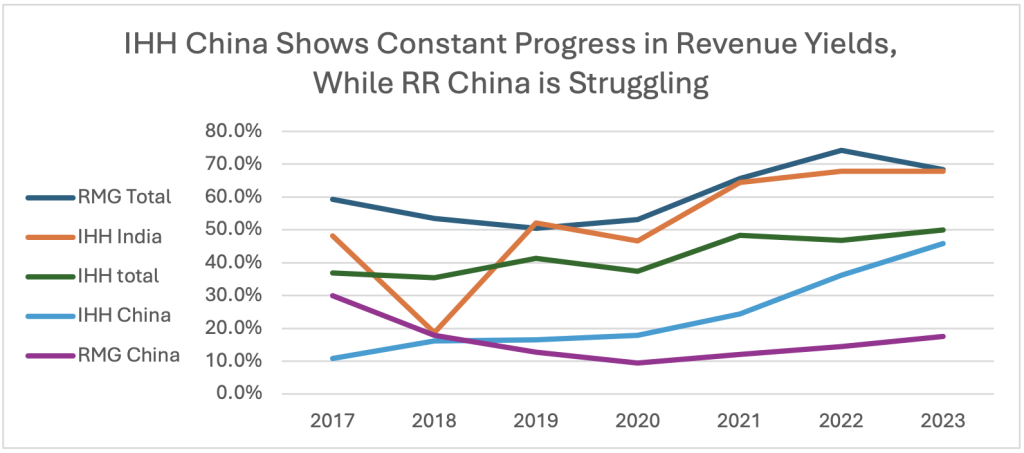

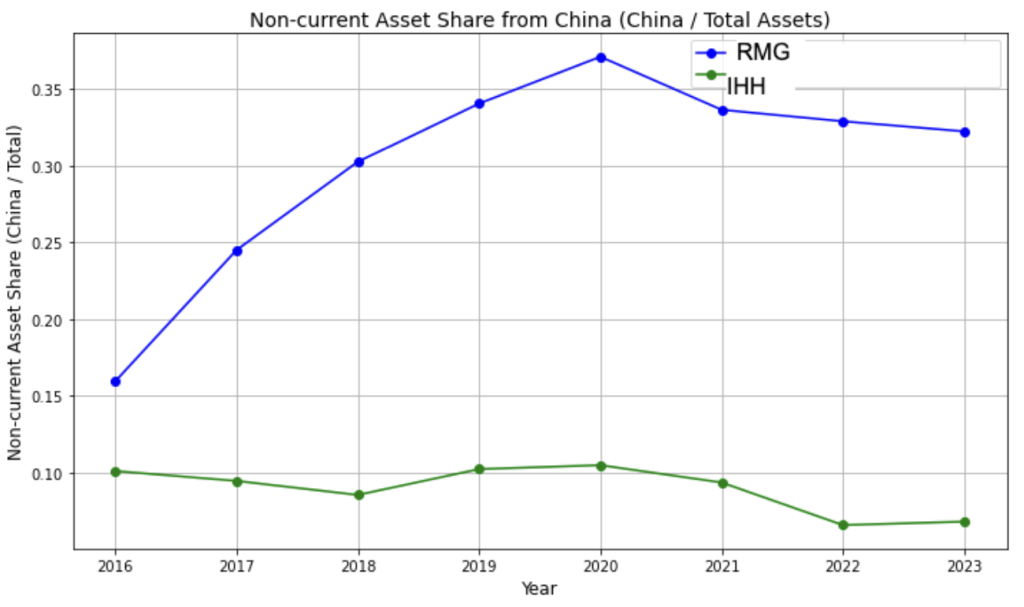

As of the end of 2023, Greater China accounts for a substantial one-third of RMG’s non-current assets, while the Singapore home market constitutes the remaining 66%. Despite this large allocation, the performance of RMG’s China segment has been disappointing. Revenue generation from non- current assets has remained low (below 20%), accompanied by significant accumulated EBITDA and net losses. In contrast, IHH Healthcare, a competitor, has seen steady progress in its China operations, with a respectable 45.8% revenue yield by the end of 2023. IHH also achieved EBITDA profitability in China in 2023. Despite this, IHH has been reducing its investment exposure in China since 2020, reallocating capital to more profitable markets such as Singapore, Malaysia, Turkey, and India.

Unlike IHH, RMG has been less transparent about the performance of its China segment, including details on annual EBITDA, net losses, and balance sheet figures. The company has often cited the “growth phase,” COVID-19 challenges, and “gestational losses” as reasons for its underperformance. Additionally, RMG has faced instability in senior leadership, including within its China segment, with executives frequently exiting without official announcements. Notably, the China CEO left RMG in August 2024. RMG CFO (Ms Goh Ann), who moved to the China segment as deputy CEO in 2020, resigned less than a year later and returned to Singapore-based property company, CDL. In September 2021, CDL Singapore fully wrote down its ~S$2 billion investment in China to just $1.

It is time to stop the destruction of shareholder equity in China segment and cease throwing good Singapore dollars after bad RMB investments. Growth must be sustainable and profitable, which can be achieved by focusing on RMG’s home market of Singapore and RMG’s core competencies. It is time to come clean and provide the detailed reporting about RMG’s China segment (similar to IHH).

Leadership Flux at Raffles Medical China, Raffles Health Insurance and RMG Group

Goh Ann Nee left CDL and joined RMG as Group CFO in 2016. In 2020, Ms. Goh left RMG, and the Group appointed Ms. Sheila Ng as Group CFO from March 2020. Ms. Goh was then appointed Deputy Managing Director of Raffles China Healthcare Division. Interestingly, RMG did not announce that she had subsequently left the company. Why did Ms Goh leave RMG (ref)?

Less than a year later, in January 2021, Ms. Goh reappeared as Chief Transformation Officer in the Executive Chairman’s office at her former employer, CDL. She led a special working group at CDL to evaluate options to improve the liquidity of CDL’s investee company, Sincere Property Group, in China. In the end, in September 2021, CDL sold its stake in Sincere Property Group for US$1, effectively ending its tumultuous backing of the cash-strapped Chinese developer. In total, CDL had invested about US$1.4 billion into Sincere in China.

In 2021, after returning to Singapore’s CDL Property Group, she played a key role in writing off CDL’s investment in its China subsidiary (Sincere Property Group), reducing it to just $1 (picture source: The Straits Times)

Dr. Vincent Chia joined RMG in February 2020 as Deputy Managing Director of Raffles China Healthcare. He was subsequently appointed Managing Director of Raffles China Healthcare in 2022. As recently as RMG Annual Report 2022, Dr. Chia was listed as part of senior management. However, based on his LinkedIn profile, Dr Chia left RMG China in March 2024. During 2024 AGM or in any SGX announcements, there was no update regarding the leadership changes in China.

The same lack of communication is evident with the loss-making health insurance business. Ms. Juliet Khew, Deputy Managing Director of Raffles Health Insurance, was listed as part of senior management in the 2023 annual report. According to her LinkedIn profile, Ms Khew left RMG in August 2024. Ms. Khew joined RMG as General Manager of Raffles Insurance in February 2020 and remained in that role until February 2022.

Most recently, the Group CFO Ms Sheila Ng left RMG on 10 November with immediate effect.

In summary, in the 2023 annual report released earlier this year, there were 10 executives in the senior management. Now RMG website (rafflesmedicalgroup.com/our-group/about-us/management/senior- management/) shows 6 members only, indicating high senior executive turnover at RMG.

RMG in Greater China

In mid-2016, the Group announced that it would spend S$1 billion over the next three years to set up hospitals and clinics in Asia, with about S$600 million to be used to spur growth outside its Singapore base, particularly in China. “Asia is growing,” Dr. Loo said at the time. “Maybe we are talking about slower growth, but it is still a plus compared to Europe and the US. There is great demand in China, and margins would not be inferior.”

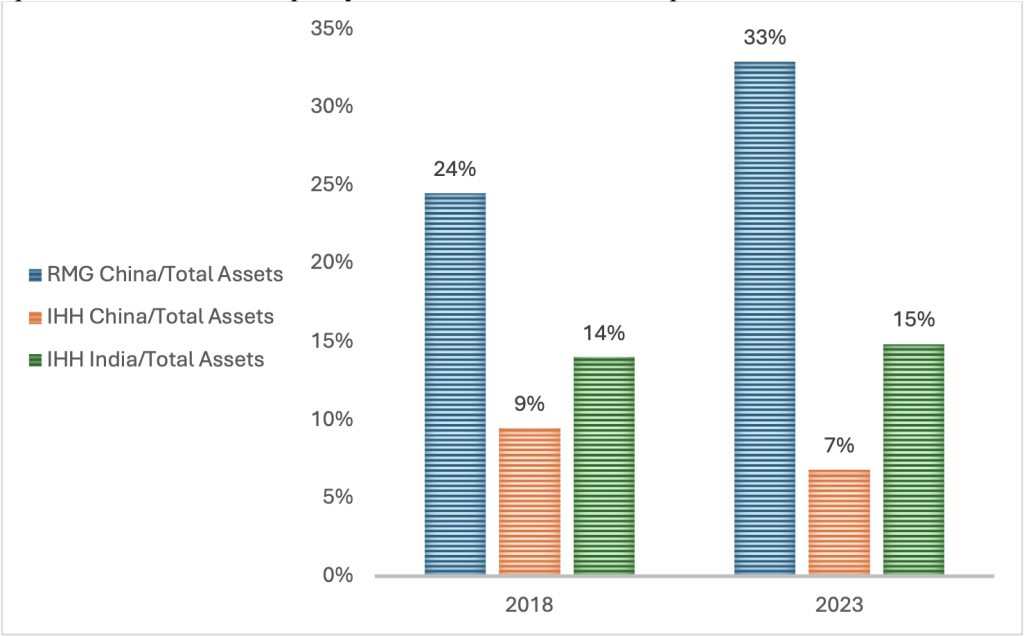

Since 2016, RMG has invested significant funds into China (in Chongqing, Beijing, and Shanghai) without providing sufficient transparency regarding profitability or investment quanta. Greater China accounts for approximately one-third of the Group’s total non-current assets (at S$340m as of the end of 2023), together with consistent and massive annual losses in this market. As of the end of 2023, RMG Group generated $0.92 in revenue in Singapore, compared to a meager $0.175 in revenue in Greater China for each dollar of non-current assets (Table 1).

Compared to RMG Group, its peer (IHH Healthcare) has consistently improved its revenue generation per invested non-current assets (revenue yields) since 2018 in China, despite the COVID obstacles (Table 2).

RMG’s China operations have been making consistent losses, even as its asset base in China continues to grow. This suggests that while RMG has been pouring more money (main in the form of equity) into China, these investments are not delivering commensurate returns, especially since EBITDA and net profits are hopelessly negative. The growing asset base doesn’t seem to translate into profitability or meaningful increase in revenue/non-current assets yield, which is a major concern.

RMG shareholders require transparency from the Group regarding the balance sheet and profitability metrics for its China hospitals (including market EBITDA and net losses), as well as detailed information about the annual investments made in this market over the past decade. RMG Group continues to withhold EBITDA details and frequently blames COVID-19 for subpar results.

In contrast, its local competitor, IHH Healthcare, has been regularly reporting its Greater China EBITDA results, showing consistent progress despite COVID-19 challenges, including a first-time EBITDA profit of 74.5 million Malaysian Ringgit (about 22 million SGD) in 2023 (Table 3).

RMG should focus on growing its profitable businesses, such as in Singapore. In 2023, RMG generated a respectable S$0.92 revenue per S$1 of its non-current assets in Singapore, compared to IHH Healthcare’s S$0.34 revenue per S$1 of non-current assets.

IHH Healthcare’s operations in China appear to be far more efficient than RMG’s. RMG may need to urgently reconsider its investment strategy in China, as the large asset base and consistent revenue growth aren’t being translated into financial success. This calls for de-risking its operations and possibly scaling down RMG’s exposure in China, where the returns on investment have been hugely negative. IHH, meanwhile, seems to be on a more sustainable growth trajectory in China. Furthermore, IHH Healthcare has been decreasing its exposure to China in favour of profitable markets (Malaysia, India and Türkiye).

Greater China hospital and healthcare operations performance comparisons: RMG vs IHH Healthcare

Tackling the continuing annual losses at RMG’s Greater China operations and derisking can increase the Group’s ROE and ROA; and thus, improve RMG’s lagging share performance.

Several factors are contributing to the challenges in Greater China: the ongoing property market collapse, trade wars, the exodus of expatriates post-COVID, intense local competition in healthcare, a depreciating local currency against the SGD, the “common prosperity” initiative, deteriorating local regulations, and weak consumer confidence. As a result, fewer individuals in China can afford the premium services the Group offers. While pandemic-driven revenue growth in Singapore once helped subsidize these Greater China losses, it is now time for an urgent strategic review.

While RMG aims to serve the expat community in China in everything, including in tertiary and specialty medicine, Raffles hospitals in Beijing, Chongqing and Shanghai have no Google Maps pages at all or GM pages with a few reviews!

IHH Group China developments, and Group’s profitable growth strategy

IHH China’s two main hospitals include the 500-bed Gleneagles Hong Kong and the 100-bed Shanghai hospital, which has a local equity partner holding 30% equity through Taikang Insurance China. In contrast, RMG Group has invested in hospital operations in China without a local equity partner, aiming to de-risk its investments. IHH opened Gleneagles Chengdu Hospital in 2017, recorded an impairment loss of 166 million RM in 2021, and subsequently realized a gain of 116 million RM from the hospital’s disposal in Q1 FY2023.

IHH also opened Gleneagles Hong Kong Hospital in 2017, which became EBITDA-profitable in May 2021, during the height of the COVID-19 pandemic.

Parkway Shanghai Hospital, which began construction in 2017 and continued through 2020, became operational in a limited capacity in 2022 and recorded an impairment loss of 353 million RM in 2022.

Based on IHH Group CEO Dr Nair-led team’s latest strategy, IHH Group will be adding about 3,800 beds – an additional 33% capacity – over the next 5 years, mostly in its profitable markets of IHH India, Malaysia and Türkiye. IHH group has identified “brownfield” expansion as the best option, given its faster ramp up, recruitment of doctors and lower CAPEX of between 30% and 40%. Note that “greenfield” hospital building typically takes around 3-5 years to achieve EBITDA breakeven (compared with between 6 and 18 months for “brownfield” hospital expansion).

Previously, RMG has considered expanding the hospital operations to Malaysia. In December 2004, RMG pulled out of its proposed acquisition of Malaysia’s Penang-based Island Hospital Sdn Bhd for RM 110 million, as RMG and Island Hospital could not resolve issues related to due diligence, according to Dr Prem Kumar Nair, who was then RMG’s General Manager of Business Development.

Twenty years later, in September 2024, under the leadership of IHH Group CEO, Dr Prem Kumar Nair, IHH’s indirect unit, Pantai Holdings, signed an agreement to acquire Island Hospital in Penang for an equity consideration of RM 3.92 billion in cash. Notably, Penang accounted for half of Malaysia’s 2023 revenue from medical tourism, which was valued at US$444 million. (ref).

In summary, RMG can and should learn a lot from the experiences of its competitors, including IHH Healthcare, to generate profitable growth in local and overseas markets, and to cut exposure to loss- making and challenging markets.

Investing in China’s Healthcare After COVID19 – Foreign Private Hospitals

In recent years, China’s healthcare sector has faced significant difficulties. In an effort to lower medical costs amidst slowing economic growth, the Chinese government has targeted corruption within the healthcare system. By August 2023, over 170 hospital administrators were under investigation, and several Chinese healthcare companies withdrew their IPO plans. The sector has seen a staggering $142 billion in market value wiped out. This crackdown aligns with Xi Jinping’s “common prosperity” initiative, which aims to reduce inequality and address the rising cost of living in China (ref. ).

Moreover, hospitals in China were once able to mark up pharmaceutical products, allowing them to generate healthy profits. However, the 2020 reform of centralized drug procurement forced thousands of private hospitals into bankruptcy, while government subsidies to public hospitals further disrupted the market.

Thanks to strong revenues and earnings in Singapore, as well as COVID-19-related government support in 2021 and 2022, RMG’s financial drain from Greater China was less noticeable. However, with higher interest costs and challenges in the Group’s Singapore market (such as high staff turnover and regional competition for medical tourism), RMG must urgently address its Greater China operations to ensure Group’s sustainable growth.

It is time to slow and reverse the unchecked destruction of shareholder value caused by funnelling after-tax profit cash generated in Singapore into Greater China solely for the sake of showing growth at all costs.

RMG Management and Board of Director need to conduct an objective strategic review of its China investments and stop throwing good money after bad. Tackling the China drain can help the Group improve its ROE and thus its share performance further, a performance which has been stagnant since 2012! The Group should explore partnerships that can help absorb some of the risks associated with its Greater China investment, such as collaborating with local partners (e.g., China Life Insurance) for an equity stake sale.

Initiatives for Sustainable and Profitable Growth at RMG Group for All Shareholders

– Provide the audited income statement and balance sheet of Greater China operations. Avoid the fate of CDL investments in China’s Sincere Property Group.

– As 100% foreign owner of the hospitals in Greater China, carve out these hospitals into a new company. Instead of using after-tax retained SGD earnings from the Group and funnelling them into the hospitals in China, use local borrowings and bank loans in CNY to minimize interest rate risks, to optimize capital structure, and to minimize depreciating CNY currency risks. Carve out these hospitals to minimize regulatory and legal actions against RR Group.

– Focus on improving staff training and retention in Singapore (the key market) while reducing the financial resources drain, management time drain, and talent drain into the bottomless pit of loss-making Greater China operations.

– Invest in regional talent development and talent pipeline, particularly in markets like Malaysia and the Philippines.

– Increase investments in Vietnam, benefiting from manufacturing growth outside China, and in Japan, which offers a stable democracy and attractive yen levels.

Invest in local marketing and business development offices in Dubai (UAE) and Kazakhstan to tap into high-value customers from the GCC (Gulf Cooperation Council) and CIS (Commonwealth of Independent States).

– Cooperate with other Singapore-based companies for synergies (for example, with Catalist- listed Don Agro for medical tourism. Don Agro has recently acquired cancer treatment-focused Евроонко [Euro-Onco] clinics in Russia).

– Tackle the key person risk: a strategic overview and business streamlining are even more urgent given the looming succession planning issue, as Executive Chairman and majority shareholder Dr. Loo, at 75 years old, is nearing retirement.

References

China: A Crackdown Comes for Healthcare

https://www.thewirechina.com/2024/02/11/a-crackdown-comes-for-healthcare-chinese-healthcare- industry/ The Wire China (2024)

City Developments (CDL): More “G” Please. Professor Mak Yuen Teen

https://governanceforstakeholders.com/2021/01/05/city-developments-more-g-please/

Penang’s medical tourism industry in good shape as Indonesian patients flock there

https://www.straitstimes.com/asia/se-asia/penang-s-medical-tourism-industry-in-good-shape-with-the- bulk-of-patients-from-indonesia Straits Times (2024)

Raffles Medical buys Penang’s Island Hospital for RM110mil

https://www.thestar.com.my/business/business-news/2004/10/26/raffles-medical-buys-penangs- island-hospital-for-rm110mil/ The Star Online (2004)

IHH poised to grow its global presence

https://www.thestar.com.my/business/business-news/2023/12/12/ihh-poised-to-grow-its-global- presence The Star Online (Dec 2023)

IHH Healthcare to acquire Malaysia’s Island Hospital for $901 million

https://www.channelnewsasia.com/business/ihh-healthcare-acquire-malaysias-island-hospital-901- million-4585666 CNA (2024)

Don Agro unit to acquire stakes in Russian oncology clinic business for 3 billion roubles

https://www.businesstimes.com.sg/companies-markets/don-agro-unit-acquire-stakes-russian- oncology-clinic-business-3-billion-roubles The Business Times (2024)

By viewing material on this website you agree to our Terms.

View and/or Use of Sakura Research materials is at your own risk.

THE RESEARCH REPORT EXPRESSES SOLELY OUR OPINIONS.

SakuraResearch.com

medium.com/@SakuraResearch

Contact info {at} SakuraResearch {dot} com

https://x.com/sakuraresearch