Raffles Health Insurance: Capital-Intensive Operations with High Risk and a History of Losses.

Sakura Research is LONG RAFFLES MEDICAL GROUP (SGX:BSL).

We think that the fair value of RMG shares should be greater than S$2.60.

TERMS APPLY.

OPINIONS ONLY.

The Group’s Founder/Executive Director and the majority shareholder, Dr Loo Choon Yong, has been Chairman of Raffles Health Insurance Pte Ltd (RHI) for many years now. In our earlier report, we covered the recent high turnover among the executives of the Group’s senior management. The same meagre communication is evident with the loss-making health insurance/reinsurance business arm (RHI). Juliet Khew, Deputy Managing Director of RHI, was listed as part of senior management in Group’s 2023 annual report. According to her LinkedIn profile, Ms. Khew left RMG in August 2024. Based on SGX announcements, there have been no updates regarding leadership changes at Raffles Health Insurance. Ms. Khew joined the Group as General Manager of RHI in February 2020 and remained in that role until February 2022.

During a recent AGM, RHI’s business model was compared to that of Kaiser Permanente, a non- profit organization in the United States, where the Group combines healthcare insurance with integrated medical services to deliver high-quality care. RHI claims that by offering healthcare insurance and providing access to its own medical facilities, it can pool risks and leverage cost advantages as the owner of those facilities. Specifically, RHI asserts that it can offer better care to its insured individuals and corporate clients while controlling costs by utilizing its in-house medical services, which are covered under the insurance policies it provides.

However, questions remain about the validity of RHI’s claimed cost advantages. RHI’s hospitals are positioned as premium healthcare providers with high operational costs, particularly in terms of staffing costs. Given that RHI has been operating for nearly two decades, can the Group provide empirical evidence to support its claims of cost efficiencies? A peer comparison analysis, including data on operating margins, staffing costs, and overall efficiency, would help substantiate these assertions. As shareholders, we do hope RMG management does not intend to operate RHI as a loss-making or barely-profitable non-profit operation, similar to U.S. non-profit Kaiser Permanente.

Furthermore, we have concerns regarding the capacity and expertise of the RHI insurance team. The insurance business is inherently complex and risky, with numerous factors that can impact performance. There is a growing perception that RMG management may be overextending itself in an attempt to drive revenue growth at all costs for the Group. For instance, RHI has entered into a partnership with Bupa Global, a well-established international insurance administrator. While Bupa receives a share of the premiums collected, it appears that the majority of the claims and loss risks are being shouldered by RHI. This raises concerns about the long-term sustainability of this model and whether RHI has the necessary resources and expertise to effectively manage these risks.

Previously, RMG’s insurance revenues were combined with several other revenue streams under the broader category of Healthcare Services, which also included managed care, GP clinic services, and COVID-19 vaccination centers. This made it difficult for shareholders to analyse the performance of the insurance business specifically. However, with the adoption of Singapore Financial Reporting Standards (International) 17 Insurance Contracts (SFRS(I) 17) on January 1, 2023, RMG’s insurance business is now more transparent. We can now clearly track the revenues generated by the Insurance Services Division, which grew to a respectable S$144.5 million in 2023, an increase of 25.6% compared to S$115 million in 2022.

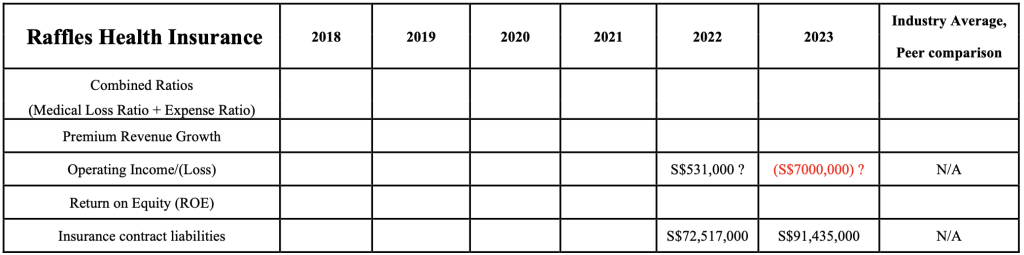

However, despite this growth in revenues, operating profits were less than satisfactory. In 2022, RHI generated a profit before tax of approximately S$531,000, with insurance contract liabilities totalling S$72.5 million. In contrast, in 2023, RHI posted a loss of approximately S$7 million before tax, while insurance contract liabilities increased significantly to S$91.4 million—representing a substantial 19% of the Group’s total liabilities. These results are concerning, especially given that funding costs have risen and ‘risk-free’ government bond yields are currently above 3-4%.

Given the importance of the Insurance Services Division—accounting for approximately 20% of the Group’s total annual revenues in 2023 (total Group Revenue: S$706.9 million)—we encourage the Group to provide shareholders with more detailed insights and transparency into the performance of this segment. The segment has been in operation since 2005, and a deeper understanding of its financial health is crucial for RMG minority investors.

Key performance indicators for the Group’s Insurance segment should include, but not be limited to, the following metrics from 2018 to 2023:

Combined Ratio (Medical Loss Ratio + Expense Ratio)

Premium Revenue Growth

Operating Income/(Loss)

Return on Equity (ROE)

Insurance Contract Liabilities

We believe that transparent reporting on these metrics will help both shareholders and the Board of Directors better assess the financial position and future prospects of the Insurance Services Division. RHI was incorporated in 2004, and two decades is more than enough time for the Group to provide a clear and transparent assessment of its performance relative to the capital invested. If the Group cannot operate the Insurance segment sustainably and profitably to generate attractive risk-adjusted returns, management should consider divesting this capital-intensive, high-risk business or bring-in capable insurance partner company (such as Chubb Ltd).

Raffles Medical Group is at a critical juncture, facing frequent senior management changes, significant ongoing losses in its Greater China investments, and underperformance in its insurance business—issues that are reflected in the Group’s declining share price. In light of these challenges, greater transparency in the Group’s financial results and a strategic review of its RHI insurance business have become crucial, particularly as the company faces succession planning concerns and worsening business conditions in China.

The Group’s management must focus on sustainable growth, prioritize its most profitable operations, and concentrate on its core competencies. Achieving double-digit Return on Equity (ROE) growth, in line with industry peers like IHH Healthcare, should be a key strategic target moving forward. Based on a net tangible book value peer (IHH) comparison valuation and under-appraised prime Singapore properties ripe for mark-to-market fair value gains, we reckon RMG should be trading at a market cap of over S$5 billion, instead of its current market cap of ~S$1.6 billion only.

Team Sakura Research has great respect for the team at RMG and its long-standing history. We remain fully committed to our research-driven activism and are open to engaging with management & the BoD to help streamline operations, enhance transparency, and maximize shareholder value.

By viewing material on this website you agree to our Terms.

View and/or Use of Sakura Research materials is at your own risk.

THE RESEARCH REPORT EXPRESSES SOLELY OUR OPINIONS.

SakuraResearch.com

medium.com/@SakuraResearch

Contact info {at} SakuraResearch {dot} com

https://x.com/sakuraresearch