By viewing material on this website you agree to the following Terms. Use of Sakura Research materials is at your own risk. THIS RESEARCH EXPRESSES SOLELY OUR OPINIONS.

Having accepted our terms and conditions, feel free to view and read our full research here.

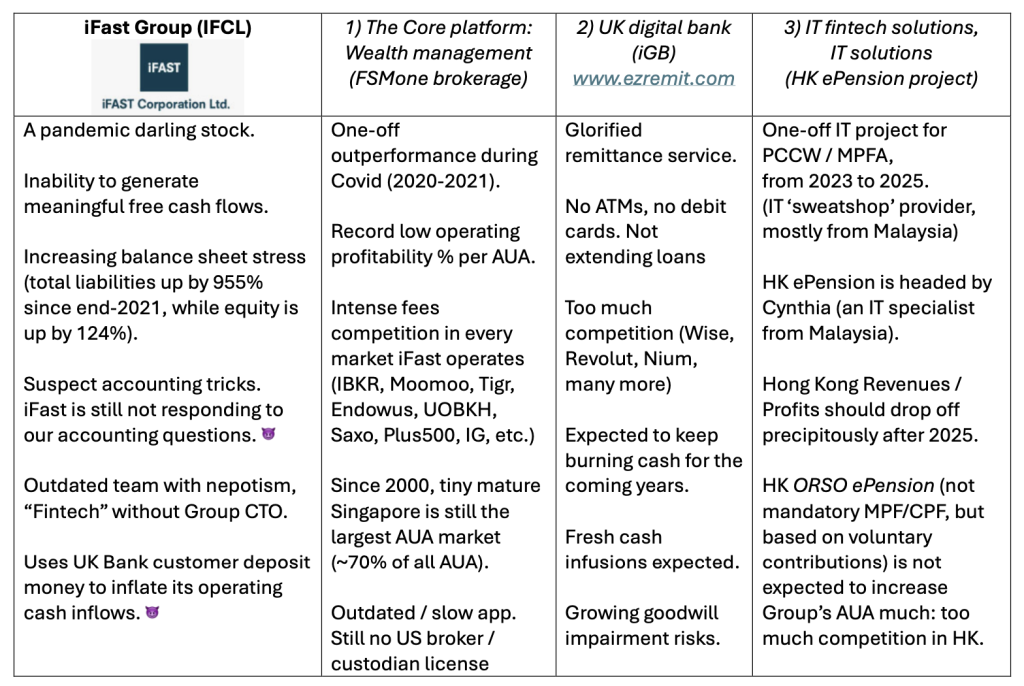

We are short iFast Corporation Ltd.

A Covid19 darling, primed for correction and underperformance.

The Group (iFast Corporation, or “IFCL”) markets itself as a global fintech and wealth management company that operates a platform for buying and selling unit trusts/mutual funds, equities, ETFs, and bonds. Retail trading and investment activity during the COVID-19 pandemic drove the platform’s exceptionally high revenue growth in 2020 and 2021. According to an article on DrWealth, the Group (IFCL) has been one of the best-performing Singapore stocks over the past decade [1].

Based on various valuation techniques, such as P/E (earnings yield), the price-to-sales ratio (P/S), the price-to-book value ratio (P/B), and free cash flow yield, the Group continues to command a substantial valuation premium. This valuation premium is even more ridiculous when compared to its global industry peers and all Singapore-listed companies with a market capitalisation above S$1 billion.

After months of analysis, we believe that the Group’s operations and performance are fundamentally misunderstood by the public, that it cannot generate meaningful free cash flows, the Group’s balance sheet shows increasing stress, and that the Group’s fair value is a fraction of its current valuation.

The Group operates online brokerage and wealth management platforms with operations in Singapore, Hong Kong, Malaysia, and China. It is also a provider of IT solutions and the new majority owner (approximately 93% ownership) of a relatively small bank in the UK. Incorporated during the dot-com era in 2000 in Singapore as an online mutual funds (unit trust) distributor, IFCL was listed on SGX in 2014. Since its founding, the Group has not been able to significantly diversify its core brokerage and distribution business beyond the small and mature market of Singapore. The island city-state accounts for more than 70% of the Group’s brokerage assets under administration (AUA), with the remaining AUA coming from customers in Malaysia, Hong Kong, and China.

We think that iFast Group is facing headwinds and negative trends in every main aspect of its business after the pandemic:

I. Struggling core Platform business with its operating profitability per AUA dropping to record lows amid intense competition in every market iFast operates.

II. Temporary revenue bump from the Hong Kong ePension IT project (2023-2025), which should drop off after 2025

III. Goodwill impairment to be recognized from the pricey UK bank acquisition, which reported losses in 2022, 2023, and H1 2024

IV. Aggressive revenue recognition, suspect total receivables growth, and possibly understated credit impairment

V. Degrading adjusted operating cash flows, which actually turned negative in Q1 2024.

VI. Survival strategy of the Group to pay more of the operating expenses with overvalued equity. The balance sheet is increasingly in distress, with total liabilities skyrocketing by 955% since the end of 2021.

VII. Stagnant senior management team with traces of nepotism and suspect governance structures

In our opinion, the Group has a massive (unfounded) valuation premium vs. its peers after a one-off COVID19 bump, despite the glaring deficiencies, complicated Group structure with diverse business areas and geographical span, increasing balance sheet stress, and inability to generate meaningful free cash flows.

#fintech #UOBKayHian #iFast #Endowus #SGX #stocks #MooMoo #Tigr #DBSVickers #FSMone #ePension #AUA

By viewing material on this website you agree to the following Terms. Use of Sakura Research materials is at your own risk.

THIS RESEARCH REPORT EXPRESSES SOLELY OUR OPINIONS.

Opinions only.

SakuraResearch.com

medium.com/@SakuraResearch

info {at} SakuraResearch {dot} com