By viewing material on this website you agree to the Terms. Use of Sakura Research materials is at your own risk.

THIS RESEARCH EXPRESSES SOLELY OUR OPINIONS.

iFast Corp recently released its FY 2024 results and there are simple but critical questions about its performance and accounting.

One single page of public accounting questions for iFast Corp.

1) Since 2021, iFAST has been providing and updating the revenue and profit guidance for your Hong Kong operations for 2023, 2024, and 2025. It is now 2025, and iFAST has still not provided any revenue or profit guidance for Hong Kong for 2026.

Is this because iFAST’s Hong Kong revenues could drop by 70-80% starting in 2026, once the eMPF (ePension) project implementation and trustees onboarding end in 2025?

Per https://www.asiaasset.com/post/24267-mpfa-0201, the Hong Kong eMPF (ePension) project implementation will last 2-3 years, ending in 2025.

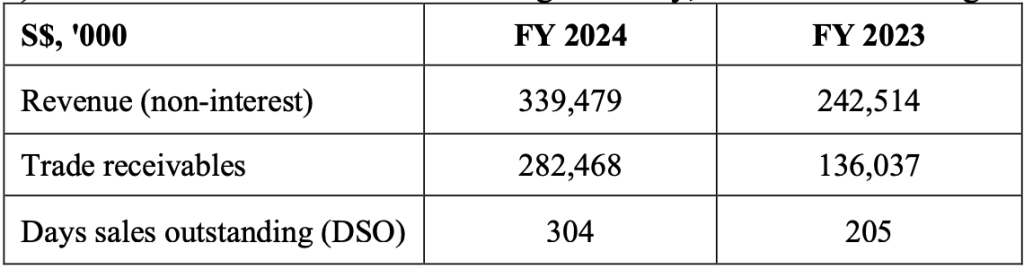

2) Trade receivables have increased significantly, more than doubling in 2024 compared to 2023. With the trade receivables at a staggering S$282 million as of 31-Dec-2024, on average, now it takes the Group about 10 months to get its invoices paid.

How is that possible?

Who are the counterparties that owe you the most money?

iFAST auditors (KPMG) have previously flagged revenue recognition policies as a Key Audit Matter (KAM), relating to both the platform AUA accrued revenues and IT solution accrued revenues. Accordingly, the calculation of accrued revenues related to both IT solutions and in-house AUA reports involves judgment and is an area of potential FRAUD risk. Revenues for any given year include accrued revenue for services that have been rendered but for which customers have not yet been billed (invoiced).

3) How do you explain the difference between iFAST UK Bank’s 2022 net loss reported in your filings in Singapore versus the bank’s filings in the UK?

iFAST annual report 2022 filed on the Singapore Exchange: S$5 million loss.

iFAST Global Bank annual report 2022 filed in the UK: ~S$20 million loss (£11.868m GBP loss)

Has iFAST underreported the UK bank’s losses?

If so, does it indicate a risk of significant goodwill impairment related to the UK bank acquisition?

Goodwill impairment is a Key Audit Matter (KAM) previously raised by the Group’s auditor, KPMG.

Source: ifastgb.com iFAST Global Bank Ltd. Annual Report 2023

4) iFAST claims to have generated amazing operating cash flow in 2024. However, the Group’s operating cash flows have been inflated by UK bank customer deposits.

Without the bank’s customer money, iFAST’s operating cash flow is actually 31 times lower than the reported figure.

The Group’s 2024 net operating cash flow, without the UK bank customers’ money, is just S$21.9 million — not sufficient to even cover the 2024 Capital Expenditures of S$26 million.

No wonder the dividend yield is well below 1%, because iFAST seems unable to generate enough operating cash flow to cover its annual CapEx and dividends.

How do you plan to grow your operating cash flow sustainably to be able to pay for capital expenditures and dividends?