Sakura Research is long Haw Par Corporation (SGX: H02).

Opinions only. Terms Apply.

- HPC Share Price: ~S$12.80

- Net Asset Value per Share (as of 31-Dec-2024): S$18.74

- Market Cap: ~S$2.8 billion (~US$2.13 billion)

- Dividend Yield: 10.8% (20¢ initial dividend, 20¢ final dividend, and $1 special dividend)

- Ex-Dividend (S$1.20) Date: May 5, 2025

- Price/Net Tangible Book Value: 0.69

- Strong Net Cash Position: S$710 million in net cash (after deducting borrowings) and S$143 millionin liquid debt instruments, together representing around 30% of market cap.

- HPC ownership of STI-30 stocks: Around 74.8 million shares of UOB (~$2.8b) and around 72 million shares of UOL Group (~$417m), representing around 113% of HPC’s market capitalization.

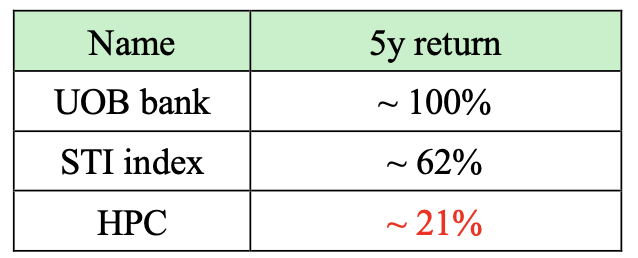

- 5-year share price performance: Terribly low 21% for HPC, compared to UOB’s approximately 100% increase and the STI Index’s approximately 62% increase.

Why Sakura Research is long Haw Par Corporation (HPC)

1) Management is Keen to Reward the Shareholders:

HPC management is now committed to rewarding all shareholders, with a final dividend of 20¢ and a special dividend of $1, resulting in an annual dividend yield of approximately 10.8%.

2) Recession-Proof Strong Balance Sheet:

HPC boasts a rock-solid balance sheet, with 30% of its market cap in cash-like instruments (cash at hand and liquid debt instruments) and nearly zero intangibles. After deducting these liquid assets, HPC’s effective market cap is around S$1.98 billion only, making it an attractive investment at current prices.

3) Own UOB and UOL Group at Subsidized Prices:

HPC provides exposure to UOB Bank and UOL Group at a significant market discount. For every 3 HPC shares, HPC investors could receive 1 share of UOB Bank and 1 share of UOL Group as dividend-in-specie. This is an excellent deal, as those 3 HPC shares cost about S$38, while the combined value of the 2 additional (1 UOB + 1 UOL) shares is ~S$43.

This arbitrage opportunity does even not account for HPC’s massive net cash plus liquid debt instruments pile (~S$850 million), its fast-growing and highly profitable Healthcare Segment, the highly valuable Tiger brand, Singapore/Malaysia commercial properties, or Underwater World Pattaya.

4) Tiger Brand and High-Growth Healthcare Segment:

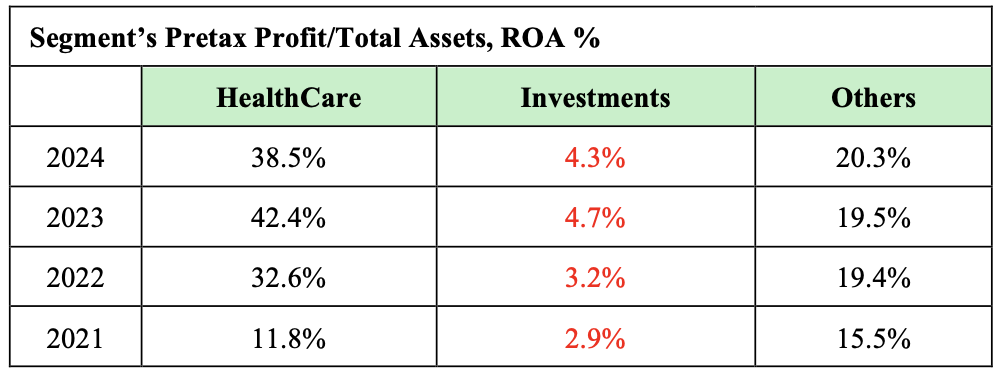

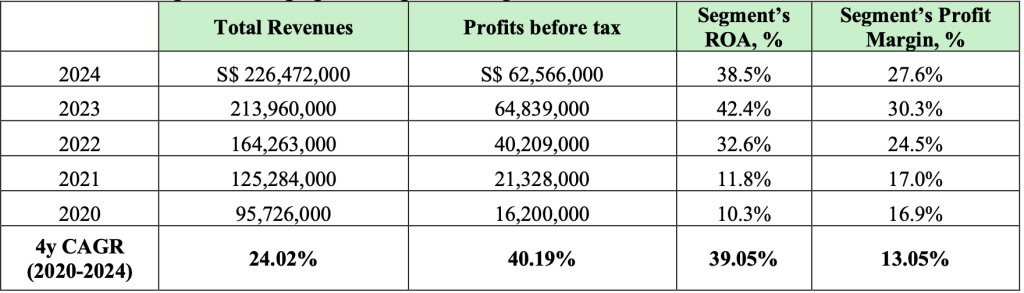

HPC’s healthcare segment is a standout, with 24% annual revenue CAGR from 2020 to 2024. This segment generates an impressive pre-tax ROA of around 40%. In 2024, the healthcare division had S$162 million in assets, generating S$226 million in sales and S$62 million in pre-tax profits. This is a high-growth, recession-resistant segment that will continue to drive the company’s profitability. This segment could be valued at S$2.3-$S2.5 billion on a stand-alone basis.

5) Limited Analyst Coverage of this Stock Gem

Despite strong operating results and an attractive dividend payout, analyst coverage of HPC remains terribly low. The most recent report was issued in July 2024, by CGS International, and it noted that HPC is trading below historical book value.

6) Opportunities to Improve Return on Equity (ROE):

Haw Par Coporations’s current Return on Equity (ROE) stands at approximately 6%, but it has the potential to increase this to at least 10%. One strategy to achieve this could be share repurchases, similar to what UOB Bank recently implemented with its $3 billion special dividend and buyback package. Increasing ROE through buybacks would create further shareholder value, but sadly, HPC’s most recent buyback was 18 years ago, in 2007.

7) Potential Stock Split to Boost Liquidity:

A stock split could increase liquidity, allowing HPC to become a likely candidate for inclusion in the SGX STI 30 Index. This could elevate HPC’s status alongside other index constituents, like UOB and UOL Group. It would also be a step toward replacing less compelling foreign companies, such as DFI Retail Group (China) and ThaiBev (Thailand), with a strong Singaporean company.

8) Simplification of the Group Structure through UOL & UOB share distributions

We believe HPC’s management should simplify the corporate structure by distributing its UOL Group and UOB shareholdings (as dividend-in-specie to Haw Par shareholders) to improve stock liquidity, management focus on ROE maximisation, and enhance its growth potential.

We remember the late Wee Cho Yaw, the great businessman and philanthropist of Singapore, with deep respect.

The Wee family is deeply involved in the management and ownership of several prominent listed Singapore companies, including: - United Overseas Bank Ltd (UOB) – One of Singapore’s top-three banks, with a market capitalization of around S$62 billion.

- UOL Group Ltd – One of the largest property companies in Singapore, with a market cap of around S$5 billion.

- UOB Kay Hian – A leading stock brokerage with a market cap of S$1.7 billion.

- United Overseas Insurance (UOI) – With a market cap of approximately S$460 million.

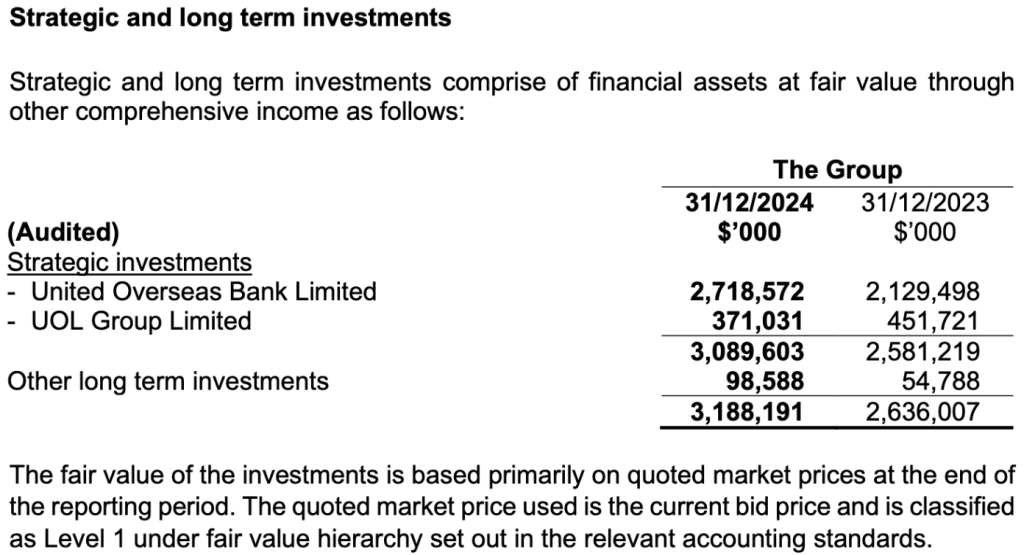

- And of course, our favourite, the Tiger Balm maker – Haw Par Corporation. These companies are intricately linked by a web of cross-shareholdings, a structure that is somewhat unusual for large Singapore-listed stocks in today’s market. For instance, HPC owns approximately 74.8 million shares of UOB (valued at S$2.7 billion as of 31-Dec-2024) and around 72 million shares of UOL Group (valued at S$371 million as of 31-Dec-2024). In turn, the UOB Bank holds about 10% of HPC. We believe that these cross- shareholdings should be simplified to increase the liquidity of HPC shares on the Singapore Exchange (SGX).

Mr. Wee Ee Lim, who has been the CEO of HPC since 2003, is also the Chairman of UOL Group since 2024.

On February 28, a news report caught our attention: “Minority shareholders request UOI to distribute Haw Par Corporation (HPC) shares, unlocking shareholder value at UOI.”

We support the shareholder activism by Ong et al. aimed at unlocking the value for all shareholders that should also increase the stock liquidity of HPC.

The structure and the cross-holdings between the companies provide a complex but potentially valuable network of assets, expertise, business support, and investments, which may offer considerable upside to shareholders if the value of these assets is more directly realized, such as through potential distributions, privatization, or strategic restructuring.

HPC operates across three key revenue-generating segments:

1) Healthcare: Manufacturing, marketing, and trading healthcare products, most notably the iconic Tiger Balm.

2) Low-ROA Investments: Investing in properties and securities, such as shares of UOB and UOL Group

3) Others: Providing leisure-related goods and services, including managing Underwater World Pattayain Thailand.

Poor share performance by Haw Par Corporation

Over the past 5 years, the performance of HPC’s share price has been poor, despite a solid, cash-rich balance sheet and highly profitable Healthcare (with ~40% ROA) and Others (with ~20% ROA) segments.

In the meantime, HPC’s largest asset – UOB shareholding (with around 74.8m UOB bank shares), has experienced about 100% in just the share price increase (excluding the UOB dividend payments). HPC’s UOB shareholding is currently valued at about S$2.8 billion, that’s near the entire HPC’s current markep cap of around S$2.8 billion dollars.

We believe that reducing the assets in the Investments segment (such as through distributing UOB and UOL Group shares) can simplify the Haw Par’s corporate structure, enhance its two highly profitable segments—Healthcare and Others,—and increase HPC’s ROA from a few percent currently to 9% ROA.

The HealthCare Segment: the high-growth, high-return segment

Let’s take a deeper look at the star growth performer of Haw Par Corporation. The ‘HealthCare’ segment products are primarily manufactured under the ‘Tiger Balm’ brand. Over the years, Tiger Balm has received multiple awards and honours and has become a household name in many countries. Leveraging on its strong brand name, HPC has introduced numerous product extensions to the Tiger Balm range, branching from its traditional ointment product to muscle rubs, plasters, back patches, mosquito repellents and neck & shoulder rubs. Tiger products are one of the best-known Singapore-grown brands, sold almost in every corner of the globe. It’s amazing recession-resistant growth performance is noteworthy.

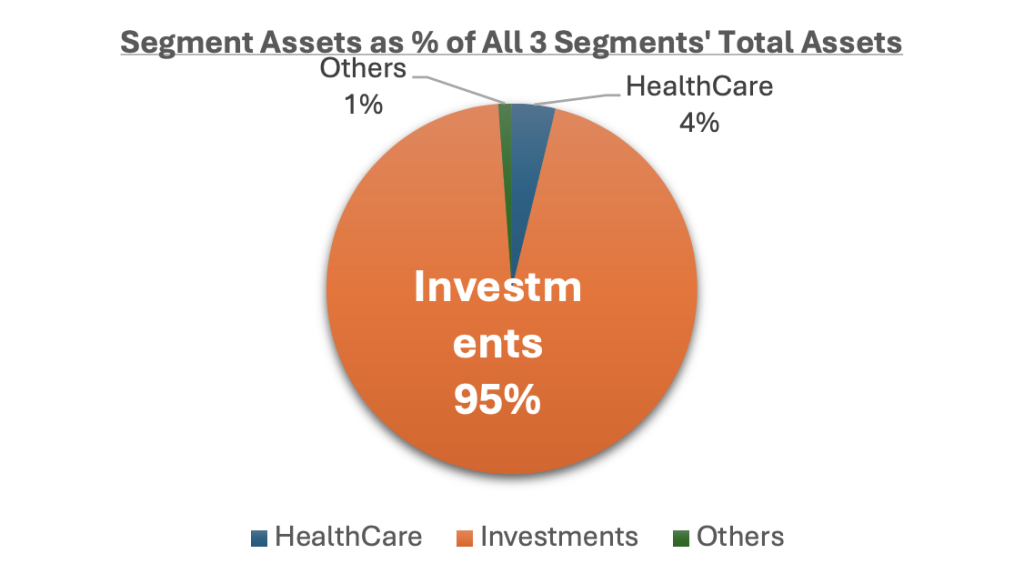

As of the end-2024, the “HealthCare” segment accounted for a mere 3.8% of all segment assets at Haw Par Corporation, yet generated 25% of total pre-tax profit of the 3 HPC’s segments taken together.

In 2024, the Healthcare segment had S$162 million in total assets, generating S$226 million in sales and S$62 million in pre-tax profits. This is a high-growth, recession-resistant segment that will continue to drive the company’s profitability in the future.

If we were to value the Healthcare segment as a stand-alone company, taking the 40 times of its S$62 million 2024 pre-tax profits, it could be valued at approximately S$2.5 billion.

If we took 10 times of its 2024 annual revenues, the Healthcare segment could be valued at approximately S$2.3 billion (especially, the highly valuable Tiger brand).

Cash-Rich Balance Sheet and Interest Income

In addition to the above-mentioned 3 revenue-generating segments of HPC, the fourth segment would be its cash holdings and investment in liquid debt instruments.

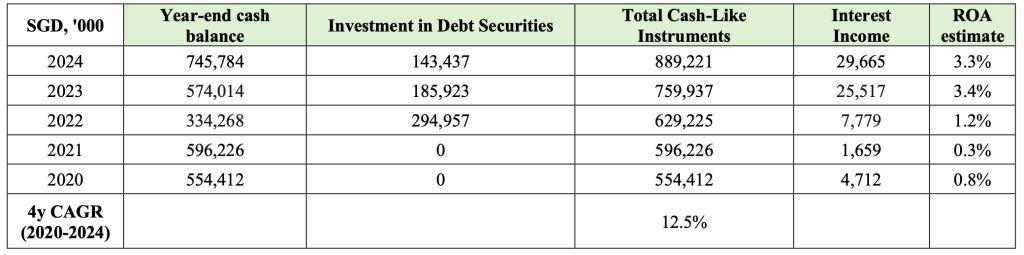

Based on our calculations, HPC’s total cash-like instruments (cash on hand and investments in liquid debt securities) have grown at a 12.5% CAGR rate from 2020 to 2024.

After deducting the total borrowings of a mere S$36 million, HPC has around S$853 million net Cash-Like Instruments on hand (about 30% of the HPC’s current market capitalization of S$2.8 billion). In 2022, HPC invested a whopping S$295 million in Singapore Government Treasury Bills. HPC’s underwhelming investing return performance is also visible based on the interest income on its growing cash pile performance. In 2024 and 2023, HPC generated around 3.3% and 3.4% return on assets based on our below calculations (Table 4).

Simplify the Corporate Structure, Reduce the Cross-Shareholdings and Distribute UOB and UOL Group Shares to Haw Par Shareholders

The UOB share investments are the largest single asset of Haw Par Corporation. We like the recent UOB share performance since COVID and we believe Haw Par Corporation gives us a nice deemed ownership of UOB shares.

HPC should simplify its corporate structure, focus on the high-growth, high-return operations, and stop being a low-return fund management/investment holding company for UOB bank and UOL Group property shares. We believe the poor share performance of HPC over the past 5 years is due to the low liquidity and complicated corporate structure of HP, with the majority of assets belonging to the Investment segment, which generates lagging pre-tax return on assets (~4.3%).

We would like to propose that HPC management distribute these shares to its shareholders as dividend-in-specie (1 share of UOB Bank and 1 share of UOL Group for every 3 HP shares held by all HPC shareholders). UOB and UOL shareholdings account for approximately 72% of HPC’s total assets, and around 113% of Haw Par’s current market capitalization of ~S$2.8 billion.

If HPC management were to distribute the UOB and UOL shareholdings to the Haw Par shareholders, this could increase HPC’s ROA to around 9%.

Given that there are around 221.4 million HPC shares outstanding, each HPC shareholder could be entitled to 1 share of UOB and 1 share of UOL Group for every 3 HPC shares they own.

For example, HPC’s CEO Mr. Wee Ee Lim now holds 29.71% and 34.88% of total number of ordinary voting shares in UOL Group and HPC, respectively. As recently as June 2024, he has increased his stake in UOL Group through market transactions. Through HPC’s distributions of its UOL shares to its shareholders, Mr. Wee Ee Lim can increase his direct stake in UOL Group further.

Call to HPC Management for Strategic Review

We have deep respect for the achievements of Haw Par Corporation.

However, over the trailing 5 years, Haw Par Corporation’s share performance (up about 21%) has been lagging the STI stock market index as well as its largest asset’s (UOB bank share price performance – doubled over the past 5 years excluding the dividends) performance. It is double disappointing that HPC shares currently trade at about 2/3 of its cash-rich net book value.

As shareholders, regulators, and authorities closely monitor HPC’s lagging financial performance and dismal stock liquidity, we urge Haw Par Corporation’s management to conduct a strategic review aimed at unlocking shareholder value, address the company’s persistent share underperformance, and closing the unjustified large market discount relative to the company’s strong cash-rich balance sheet.

Actions could include the following:

Corporate Structure Simplification: Simplifying the corporate structure by distributing UOB and UOL Group shares to HPC’s shareholders could enhance liquidity and position HPC as a more prominent player in the SGX market, unlocking further value for Haw Par investors.

Separation of High-Return Segments from Low-Return Investment Holdings: Separate the high- return segments from the low-return Investment Holdings segment to drive better performance and focus.

Based on our calculations, the highly-profitable fast-growing Healthcare Segment (mainly the Tiger brand products) could be worth $2.3 billion on a stand-alone basis.

Stock Split: A stock split would increase liquidity, improve accessibility for smaller investors, and enhance the likelihood of inclusion in the SGX STI 30 Index, strengthening HPC’s market position.

Maximize ROE: Exploring options such as share buybacks could improve HPC’s Return on Equity (ROE) and further drive shareholder returns, demonstrating a commitment to maximizing value for HPC investors.

Privatization: Since the Wee family owns the majority of shares, HPC is an attractive asset for privatization by the family members and their associates.

By taking these steps, HPC management can significantly enhance shareholder value, improve the stock liquidity, and position the company for long-term success.

Sakura Research

OPINIONS ONLY.

TERMS APPLY.