By viewing material on this website you agree to the Terms.

Use of Sakura Research materials is at your own risk.

THIS RESEARCH EXPRESSES SOLELY OUR OPINIONS.

ST Engineering Group (STE, S63.SI) – Bear Case by Sakura Research

STE Group (SGX: S63) Share Price: S$7.91

Market Cap: ≈S$24.7B (≈US$19B)

Public/free float: 48.54%

Singapore’s Temasek Fund: 51.02% ownership

Average volume (3-month): 7.65M shares (~$47m USD daily)

Short interest (as of June 13): 0.11% of Outstanding Shares

End-2024: Cash at 430m vs. total borrowings at $6,108 million

Performance: YTD +70% vs. STI index +3%. [1Y +90% vs. STI index’s +18%]

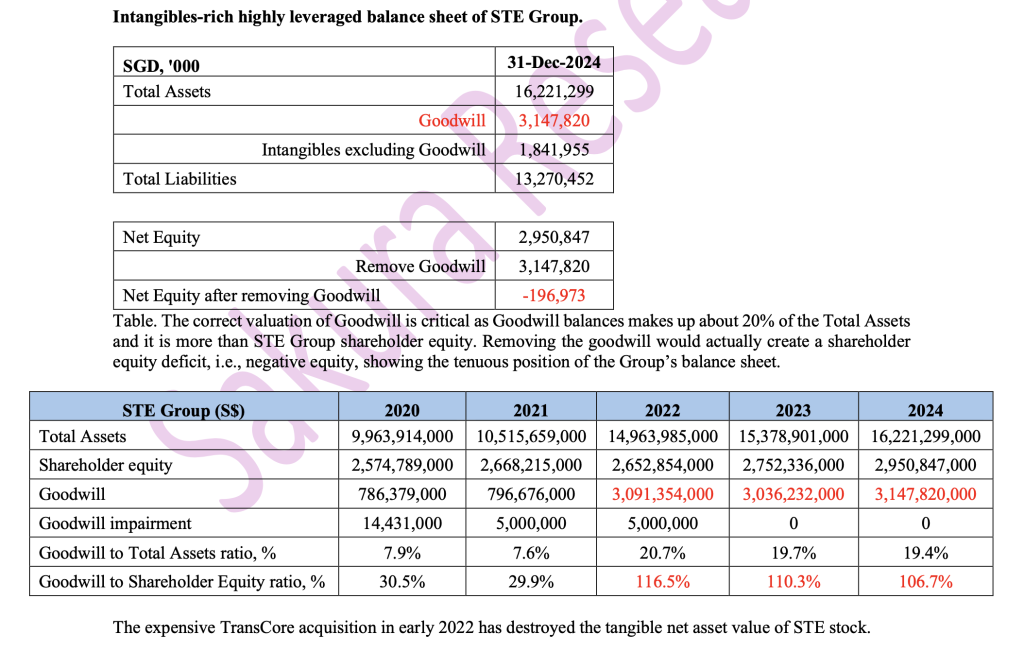

In our view, STE is an overpriced over-leveraged defence play handicapped by high debt load, high annual capital expenditure spend, negative tangible net asset value and unrecognized goodwill impairment (about S$1.7b). The Group’s reported annual net income has not been able to cover its annual capital expenditures together with its annual Dividends paid to shareholders every single year since 2015. We estimate goodwill impairment of S$1.7B resulting from US TransCore Partners acquisition in 2022, when the interest rates were at about 0%.

STE Group is an integrated engineering group with 3 segments: Commercial Aerospace (CA), Urban Solutions & Satcom (USS), defence and public security (DPS) segments. Recently, its share performance has been on a tear and we took a close look at the Group’s asset efficiency, as a whole and by each of 3 operating segments (CA, USS, and DPS).

The Group has faced a significant financial strain over the past seven years, from 2015 to 2024, running a “deficit”between net income and the combined outflows for CapEx and dividends. This suggests that the company cannot sustainably fund both capital expenditures and shareholder returns, a typical red flag for capital-intensive businesses that cannot create sustainable shareholder value. Furthermore, between 2022 and 2024 alone, the Group’s CapEx totaled approximately S$1.88B, surpassing the cumulative net income of S$1.82B in the same period.

Moreover, interest payments surged more than eightfold, from S$34M in 2021 to S$282M in 2023, a stark reflection of the increasing debt burden, exacerbated by the debt-fuelled gigantic and disastrous TransCore acquisition in 2022.

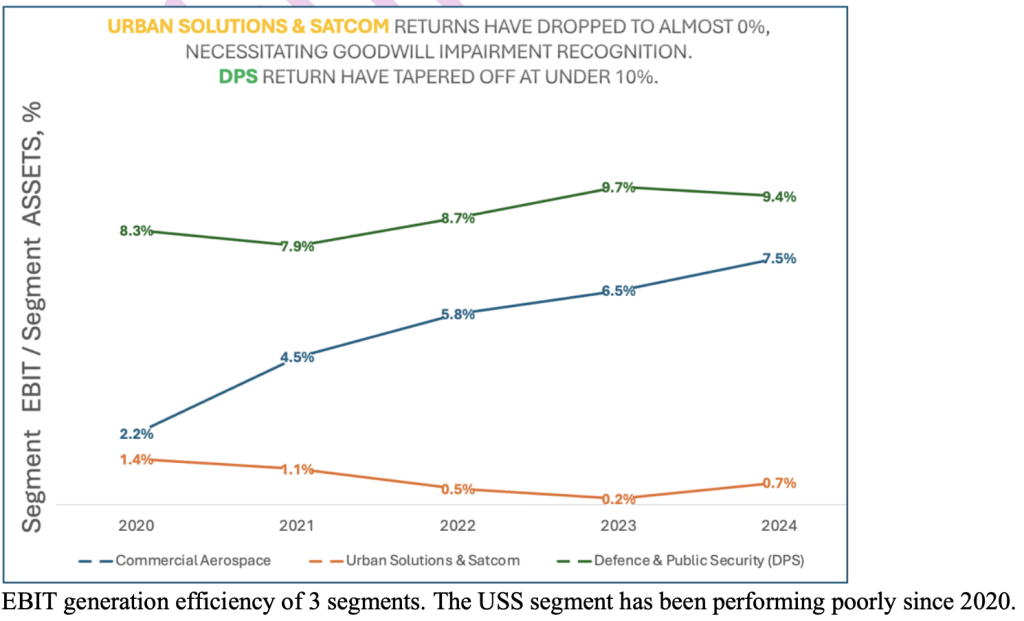

STE Group has 3 operating segments. The DPS segment EBIT (Earnings Before Interest & Taxes) returns have tapered off under 10% yield, while the Commercial Aviation segment’s EBIT/Asset yield picture is getting cloudy under the global trade wars, protectionism, higher jet fuel prices, wars, and closed airspaces with the resulting travel disruptions. We compared the Group’s 3 operating segments and their EBIT generation efficiency per segment assets. The TransCore-container USS segment EBIT generation efficiency has dropped off significantly from 2022 to 2024. Of note, TransCore (TC) Partners generated US$143 million in EBITDA in 2020, before the acquisition by the Group.

ST Engineering marks biggest-ever investment with $3.6b TransCore (TC) purchase in early 2022

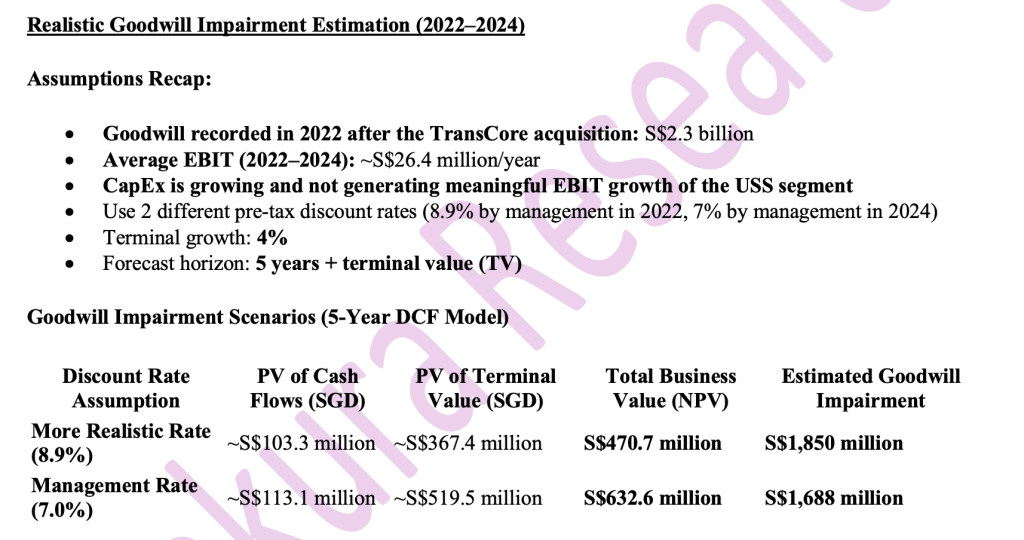

A pivotal moment for the Group’s negative performance was the overpayment for the US-based transportation and tolling tech company, TransCore, in March 2022. At that time, the Fed funds rate was around 0.50%. The Group acquired TransCore for US$2.68 billion (S$3.62 billion) at a time when financing conditions were exceptionally favorable. TC assets were mostly added to the Urban Solutions & Satcom (USS) segment, especially by adding $2.3 billion in goodwill balance.

However, the Fed funds rate has since risen significantly, now sitting at 4.25%–4.50%, placing strain on the Group’s debt-servicing capacity. While the Fed rates rose since early 2022 to 2024, STE management actually decreased the pre-tax discount rates used for S$2.3 billion goodwill valuation from 8.9% in 2022 to 7% in 2024 (this reeks of dishonesty or incompetency from the group’s finance team.). The TC acquisition was based on overly optimistic assumptions, expecting TransCore to be cash-flow positive from year one and earnings-accretive by year two. In reality, the Urban Solutions & Satcom (USS) segment, which includes acquired TransCore, posted the worst EBIT performance in 2023 since 2020.Furthermore, in January 2024, Mr Tracy Marks, TransCore President & CEO, announced his departure.

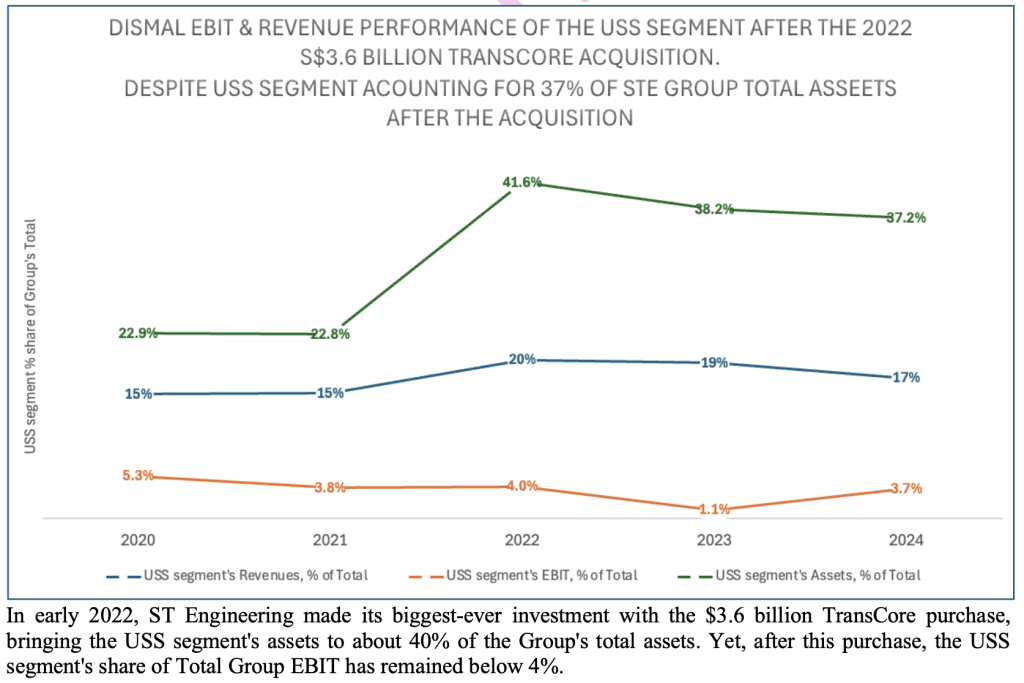

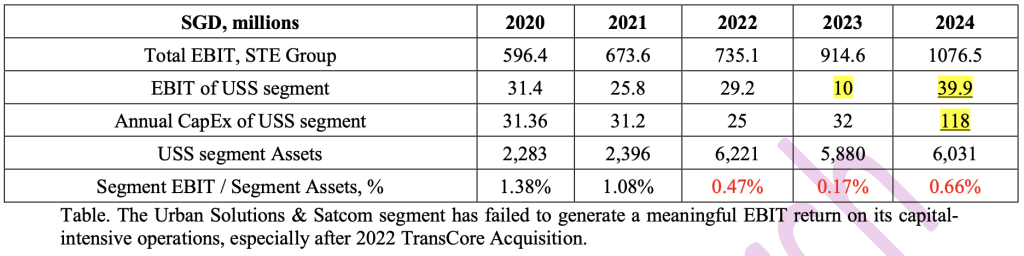

TransCore’s contribution in 2022 was S$620.6M in revenue and S$61.9M in net profit. The USS segment’s overall EBIT remained stagnant from 2020 to 2024, despite a sharp increase in USS assets—from S$2.39B in 2021 to S$6B in 2024. This represents an abysmal EBIT-to-assets yield of less than 0.7% over the same period. In other words, the Group’s investment in this USS segment has grown without delivering a proportional return. Further complicating matters, TransCore’s involvement in the US infrastructure sector is facing increased challenges. US company Conduent is contesting the US$1.7B New Jersey E-ZPass contract awarded to TransCore, highlighting the rising protectionist sentiment against foreign-owned companies in US infrastructure procurements.

In fact, in 2023, the Group’s USS segment reported its lowest annual EBIT, at just 10 million SGD since 2020, despite the massive TransCore acquisition. TransCore’s EBITDA (earnings before interest, tax, depreciation and amortisation) was much higher at US$143 million as at end-December 2020 (before the 2022 acquisition).

We estimate a $1.7 billion goodwill impairment from the TransCore acquisition, which equals about 240% of ST Engineering Group’s 2024 net income of 702 million SGD.

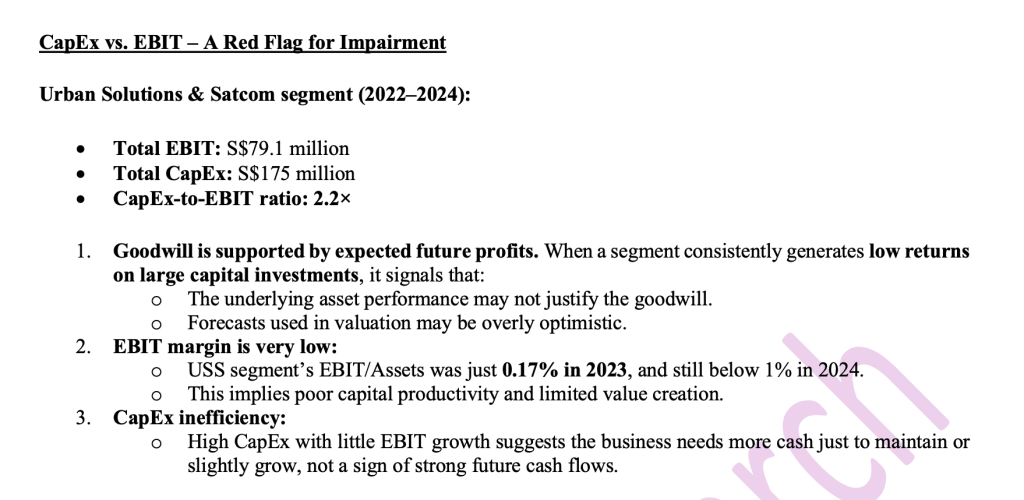

From 2022 to 2024, TransCore-containing USS segment produced approximately S$79.1 million in EBIT, while USS capital expenditures over the same three-year period totalled S$175 million—more than double the EBIT. From 2021 to 2024, the USS segment’s assets have grown by approximately 151%, reaching a staggering S$6 billion.

The Group has recognized about S$20 million total goodwill impairment for 2020 and 2021, with on about $800 million goodwill on its balance sheet prior to TransCore acquisition. After TC acquisition, from 2022 to 2024, it has recognized just S$5 million in goodwill impairment on a much larger $3.1 billion goodwill balance. We estimate about $1.7 billion in goodwill impairment to be recognized by STE (about 7% of its current market capitalization,or about 2.5 times of its 2024 annual net income of S$702 million).

Difficulty converting rising order book values to net income.

On March 3, the Singapore government announced a 12.4% increase in its defence budget for FY2025, bringing total defence spending to S$23.4 billion. The hike is intended to support projects that were deferred or disrupted due to COVID-19. However, then Defence Minister Ng Eng Hen noted that such increases will moderate inFY2026, as the government aims to keep defence expenditure within 3% of GDP (ref).

While the Group’s reported order book has grown approximately 85% from 2020 to 2024, net income over the same period has increased by only 35%, implying a modest compound annual growth rate (CAGR) of around 7.55%. This highlights the ongoing challenge of translating order book growth into high net income yields—largely due to the Group’s elevated borrowing levels and associated interest costs.Compounding these issues, the World Bank recently cut its global growth forecast for 2025 from 2.7% to 2.3%,citing rising tariffs and increased geopolitical uncertainty as significant headwinds for most economies.

Additionally, persistent high oil and jet fuel prices—along with restricted access to major airspaces such as Russian and Iranian—are expected to lengthen flight durations and negatively impact airline profitability.In this challenging macroeconomic environment, protectionist trade policies by major economies may become more common, further dampening global demand.

Reflecting some of this pressure, STE reported Q1 2025 revenue of S$2.9 billion, a 1.8% decline from Q4 2024.

The Group faces significant working capital pressure, particularly during periods of economic downturn, recessions, or credit tightening. Despite STE management’s focus on AI, GenAI, and increasing defence spending, the Group remains highly capital-intensive, with low asset returns and a highly leveraged balance sheet.

In conclusion, the Group’s growing financial strain—compounded by a poorly executed acquisition, poor EBIT generation and a stressed balance sheet, signals that difficult financial decisions are imminent. These may include dividend cuts, capital raises, or a restructuring of operations (such as the recent disposal of the entire equity interest in US-based construction player LeeBoy from STE Group’s DPS segment for US$290 million to pay down STE Group’s massive debt pile).

By viewing material on this website you agree to our Terms.

View and/or Use of Sakura Research materials is at your own risk.

THE RESEARCH REPORT EXPRESSES SOLELY OUR OPINIONS.

Opinions only.

SakuraResearch.com

medium.com/@SakuraResearch

Contact info {at} SakuraResearch {dot} com

https://x.com/sakuraresearch