We are short IFAST Corp (SGX:AIY).

SEPTEMBER 16, 2024.

TERMS APPLY. FULL REPORT @ https://SakuraResearch.com/

OPINIONS ONLY.

UPDATE ON IFAST GLOBAL BANK

iFast completed 100% acquisition of EPHL (Eagle Peak Holdings Ltd), taking full ownership of iFast Global Bank (iGB). Let’s take a closer look at this acquisition and iGB.

1) “Congrats” to IFAST shareholders! The UK digital bank purchase transaction, which resembles a scammy hoax, is complete!

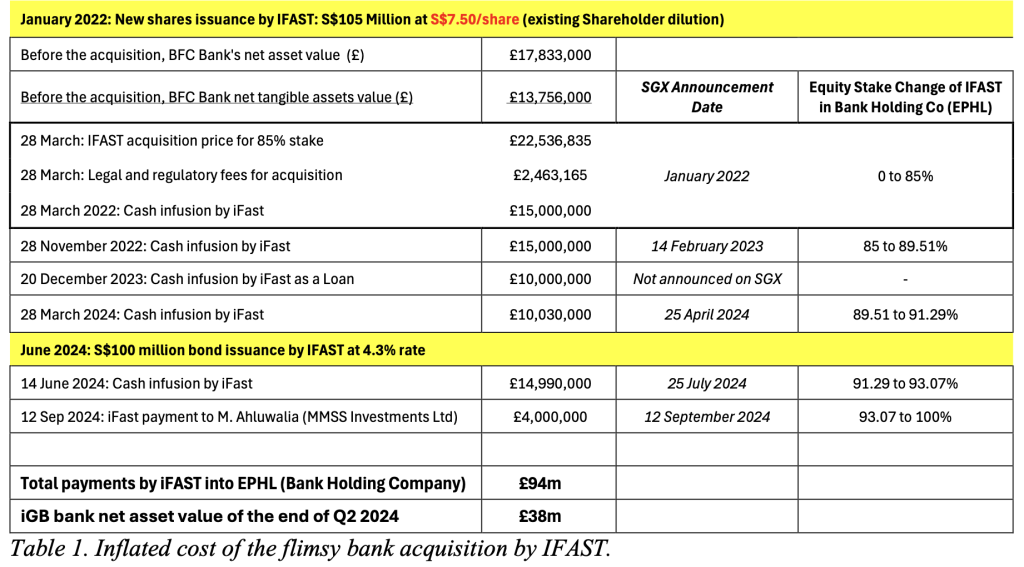

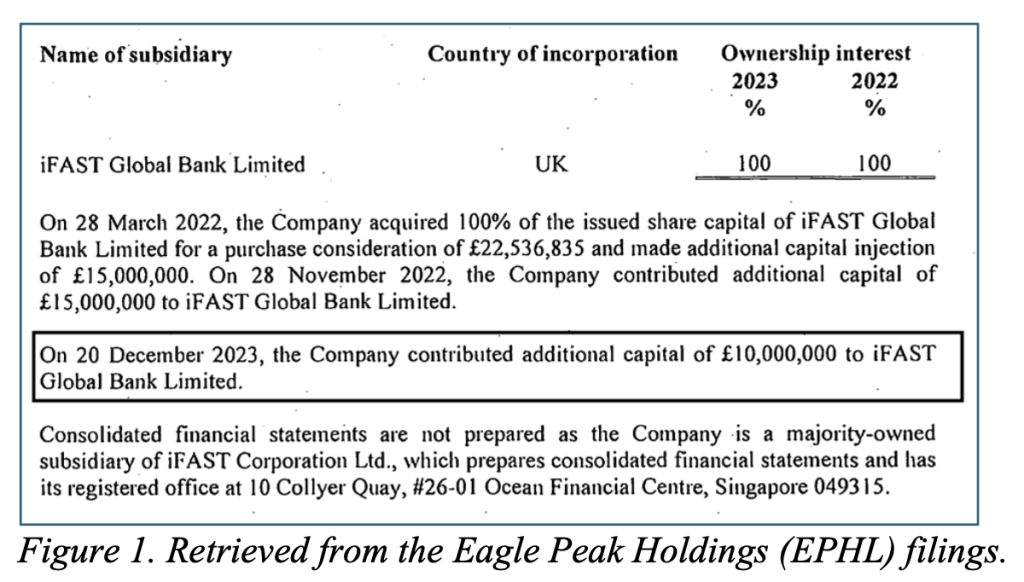

Over the past 2.5 years, IFAST has spent around £94 million (a whopping S$160m, £84m in equity and £10m in loans) on a former remittance business-based BFC bank with a net tangible assets value of just £13 million before the acquisition (Table 1, Fig. 1).

It seems that the IFAST CEO/Chairman was so desperate for a banking license after failures in Singapore, Malaysia, and Hong Kong that IFAST massively overpaid for a subpar asset in the UK.

Based on our calculations, IFAST injected a massive £94 million GBP to fully acquire former BFC bank with a tangible net book value of just about £13m GBP before the acquisition.

2) The former 15%-owning minority shareholder of EPHL, Mandeep Ahluwalia (MMSS Investments Ltd), has benefited from cash injections exclusively provided by IFAST from early 2022 till September 2024, with no contributions from him.

Since March 2022, what has this minority shareholder and director, Mandeep Ahluwalia, done to earn £4 million in September 2024 and additional funds earlier (Table 1)?

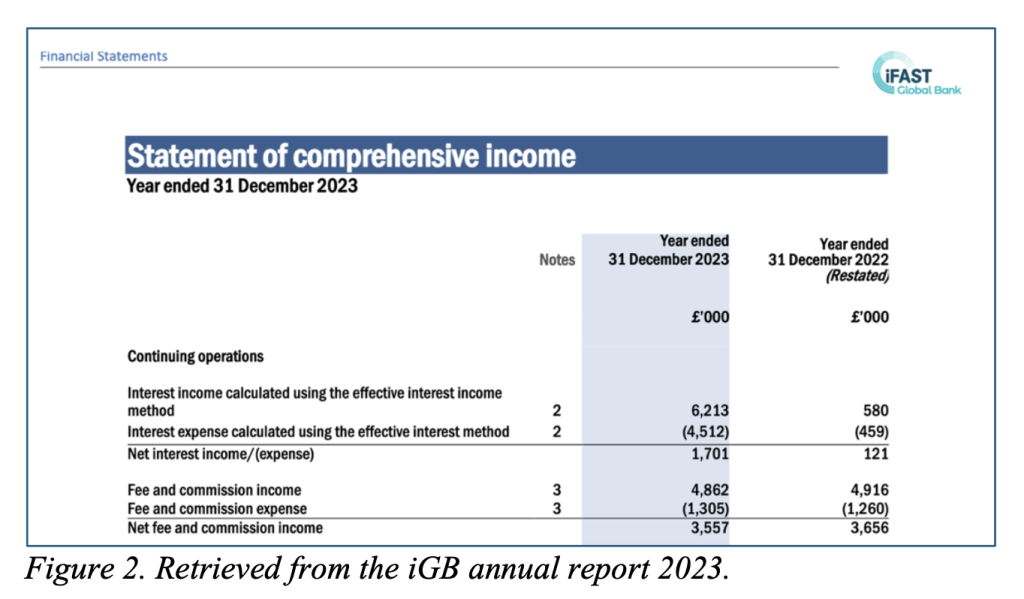

3) The iGB bank’s primary business is remittance-based fees and commissions. However, net fees / commission income has dropped from £3.656 million in 2022 to £3.557 million in 2023 (Fig. 2). This may be due to the rampant competition in the remittances sector in the UK from both traditional players as well as global fintech giants (such as REVOLUT, WISE, PayPal, etc.)

This may indicate support for our “rotten bank” hypothesis, necessitating further goodwill impairment charges at IFAST.

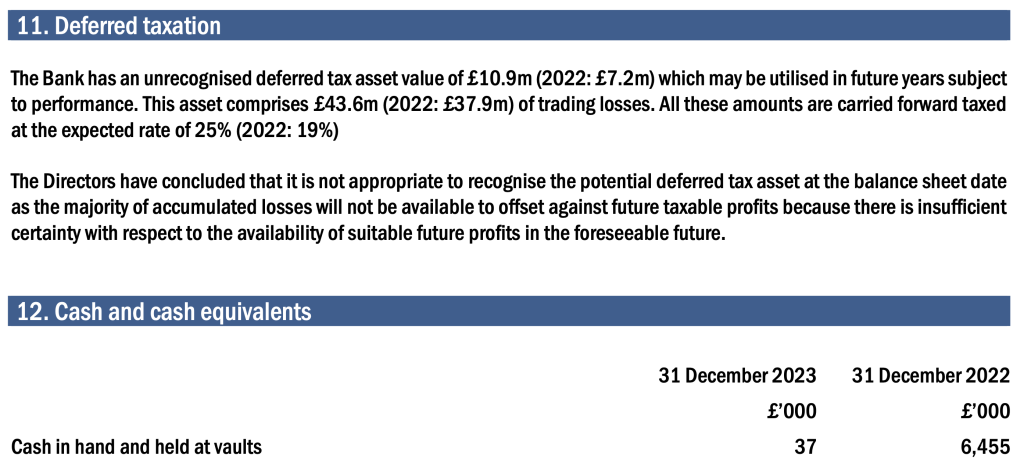

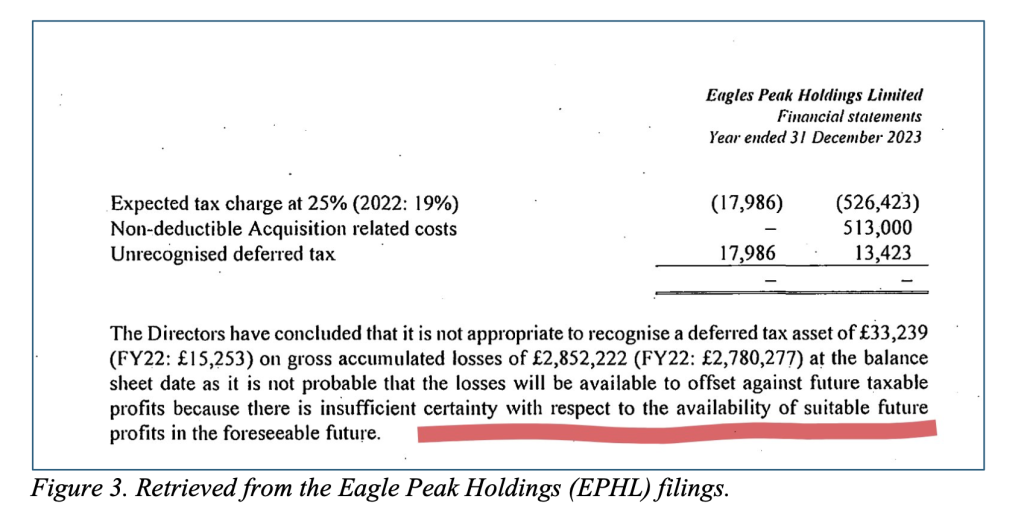

4) iFast management aims to have a profitable quarter in Q4, 2024 at its UK bank operations. Nevertheless, according to the iGB and Eagle Peak Holdings Limited (EPHL) 2023 annual reports, they do not expect meaningful profitability of iGB bank in the foreseeable future (Fig. 3). Again, this supports our “rotten bank” hypothesis, which may necessitate further goodwill impairment charge at IFAST Global Bank (iGB).

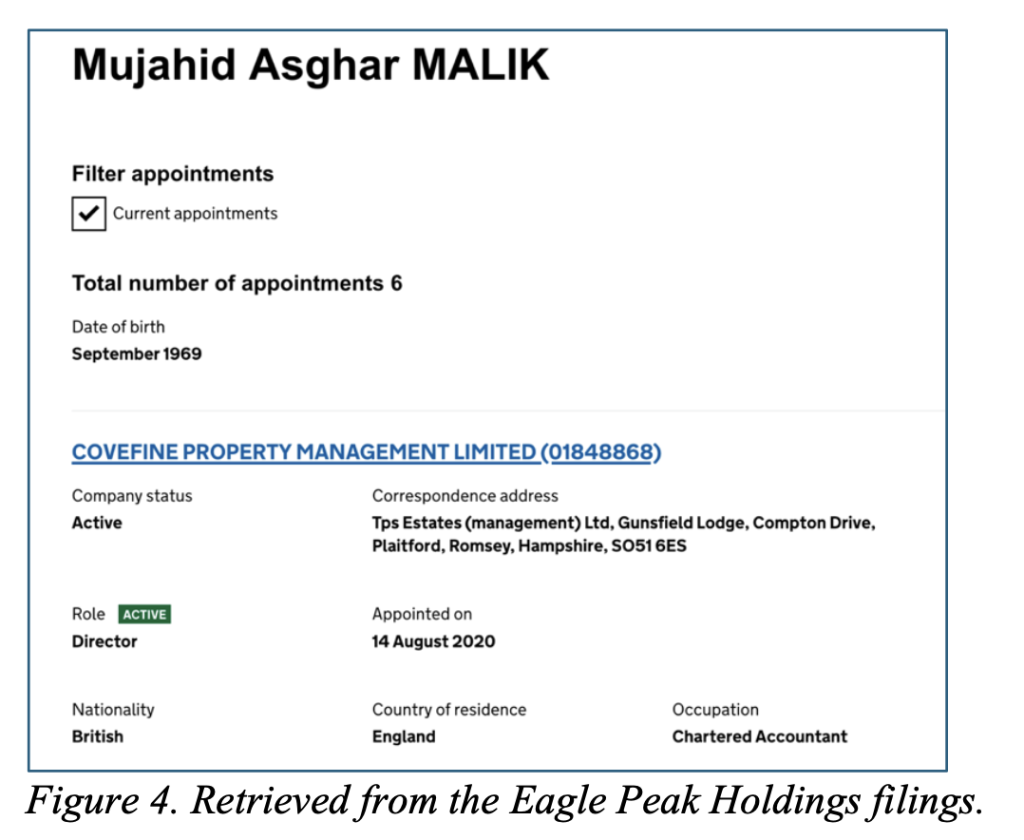

5) Interestingly, the former CEO of BFC Bank, Mr Mujahid Malik, is still the CEO of the iGB digital bank. He appears to be an accountant by training and is currently working for the following six UK companies: IFAST Global Bank Ltd, CoveFine Property Management Ltd, MRM Investments Ltd, 33 Abercorn Place Ltd, 31 Abercorn Place Freehold Ltd, and Apsley Grange Ltd (Fig. 4).

How will an outdated/stagnant and unfocused management team at iGB compete in the high-tech cut-throat fintech and digital banking global market?! Again, this probably goes to support our “rotten bank” hypothesis.

Accounting Questions about IFAST Global Bank

a) Digital banks have often been unprofitable, requiring frequent and substantial capital infusions even with world-class technology teams. For instance, Sea-owned MariBank experienced widened losses in 2023, while GXS Bank (founded in 2022 and backed by Singtel and Grab Holdings) aims for profitability by 2027.

While iFast targets iGB to breakeven & have a profitable quarter in Q4 2024, how do you even plan to operate profitably in 2025, 2026 and after, with iGB not even extending traditional consumer and/or business loans?

What is iGB’s current net interest margin (NIM) for the banking operations?

When do you expect the bank’s return rate on invested capital to exceed your inaugural $100m bond’s rate of 4.3%?

b) Based on 16-Sep-2024 update, there is a huge overpayment for a loss-making tiny bank, years of making losses, and extremely competitive environment in banking/remittances, does IFAST plan to recognize any further goodwill impairment related to this bank 100% acquisition?

How much? And why?

c) iFast aims to grow its AUA (assets under administration) to $100 billions “by 2028–2030”.

When and why did the Management decide to present the UK Bank customer deposits under the Core wealth platform’s AUA figure?

How will this affect the operating profitability % per AUA?

Customer deposits, by nature, can be removed from the UK bank at a moment’s notice. What makes iFast think that the UK bank customer deposits should be treated as Assets Under Administration (AUA) to create recurring revenues?

d) In its 2023 annual report submitted to SGX, iFast reported a total pre-tax loss for the UK bank of approximately £8 million (a sum of S$8.6 million in losses for 2022 and S$5 million in losses in 2023).

However, iFast Global Bank in the UK recorded a total loss of £17.57 million GBP for both 2022 and 2023.

Did iFast Corp understate and underreport its UK banking operations loss by around £9-10 million GBP over these two years?

It has been more than a month since we released our report on iFast and accounting questions for iFast’s response. The Original Accounting Questions are continued below:

https://sakuraresearch.com/?p=22 https://www.scribd.com/document/763110745/Accounting-Questions-for-IFAST-Corporation-Ltd

We hope that iFast management agrees to respond to our questions soon.

By viewing material on this website you agree to the following Terms.

Use of Sakura Research materials is at your own risk.

THE REPORTS EXPRESS SOLELY OUR OPINIONS.

Opinions only.

SakuraResearch.com

medium.com/@SakuraResearch

info {at} SakuraResearch {dot} com

PRESS RELEASE

Date: September 16, 2024

iFAST GLOBAL BANK (iGB): SERIOUS CONCERNS RAISED OVER RECENT ACQUISITION AND BANK MANAGEMENT

[Singapore] — iFast has completed the 100% stake acquisition in Eagle Peak Holdings Ltd (EPHL), the holding company of iFast Global Bank.

1. Completion of Controversial Acquisition: Overpayment for a Rotten Asset

IFAST stakeholders may want to take note: the UK digital bank acquisition, described as resembling a dubious transaction, is now complete. Over the past 2.5 years, IFAST has invested approximately £94 million GBP (about S$160 million) in acquiring the former remittance-based loss-making BFC Bank. This substantial spent stands in stark contrast to BFC Bank’s modest net tangible asset value of £13m before the acquisition.

This acquisition raises questions about the decision-making process at IFAST Group (SGX:AIY), particularly given iFAST’s previous failures in securing banking licenses in Singapore, Malaysia, and Hong Kong. It appears that IFAST management’s desperation for a banking license led to an overpayment for a relatively subpar asset.

2. Concerns Over Minority Shareholder Benefits

Mandeep Ahluwalia (MMSS Investments Ltd), a 15%-owning minority shareholder at the bank-holding company (EAGLES PEAK HOLDINGS LIMITED), has notably benefited from the substantial cash injections provided solely by IFAST.

Despite no financial contributions from Ahluwalia’s side, he has secured £4 million in September 2024 and additional funds earlier. This raises serious questions about the value added by this minority shareholder and director.

3. Deteriorating Financial Performance

The primary business model of iGB Bank, based on remittance fees and commissions, has seen a decline. Net fees and commission income dropped from £3.656 million in 2022 to £3.557 million in 2023. This downward trend supports the “rotten bank” hypothesis, suggesting a potential need for a further goodwill impairment charge at IFAST Global Bank.

4. Lack of Profitability in Foreseeable Future and Stagnant Management

The 2023 annual report from Eagle Peak Holdings Limited (EPHL), which holds 100% interest in iGB Bank, indicates no expected profitability in the foreseeable future (the next 3-5 years). This reinforces our concerns about iGB bank’s operations, profitable growth prospects, financial viability and supports our “rotten bank” hypothesis.

Further complicating matters, Mr. Mujahid Malik, former CEO of BFC Bank and current CEO of iGB Bank, continues to serve as CEO while also holding positions in 5 other UK companies. This raises concerns about the capability and focus of iGB’s management team in the competitive fintech and digital banking sector.

Conclusion

The unfolding issues at iFast, including the questionable acquisition strategy of iFast Global Bank, disproportionate benefits to minority shareholders, declining financial performance, and stagnant management, underscore the pressing need for transparency and accountability.

Shareholders, regulators, and stakeholders are encouraged to closely monitor developments and seek further clarifications from IFAST’s management.