Sakura Research

TERMS APPLY. OPINIONS ONLY. FULL REPORT AT https://SakuraResearch.com/

We are short iFast Corp (SGX:AIY), and long its dividend-rich & cash flow yield-rich peer, UOB-Kay Hian (SGX:U10).

Re Business Times article: iFast, analysts refute short-seller claims that business is unsustainable.

https://www.businesstimes.com.sg/companies-markets/ifast-analysts-refute-short-seller-claims-business- unsustainable

1. “In response to queries from Business Times, iFast declined to comment on most of the allegations made by Sakura Research.”

[Sakura Research]: This is telling.

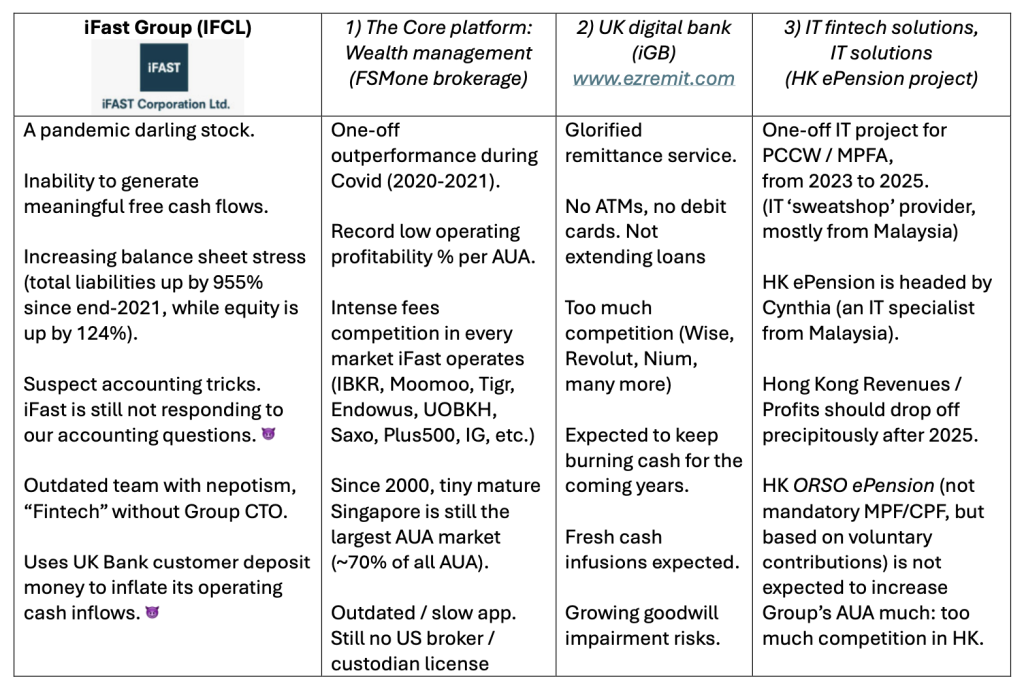

There are many critical issues regarding the increasing balance sheet stress and leverage ratio, meager operating cash flow and free cash flows, and alleged accounting tricks.

Yet, IFAST management seems to prefer burying their heads in the sand.

2. “In response to the report, an iFast spokesperson said the company has continued to guide for revenue from its ePension division to be sustained over a contract period of seven years.”

[Sakura Research]: This is a great non-answer.

Can iFast confirm that the 2026 Hong Kong target revenues will be similar to the 2025 guidance (ie, a gross revenue target of more than $1.2 billion HKD and a net revenue target of more than $1 billion HKD for 2025)?

The recent strengthening of the SGD against other currencies (HKD and USD) will negatively affect iFast’s profits from Hong Kong.

3. “iFast’s Hong Kong-based subsidiary, iFast ePension Services, launched Occupational Retirement Schemes Ordinance (Orso) e-pension services, a digital pension solution for Hong Kong Orso pension schemes in June last year.”

[Sakura Research]: The so-called ORSO ePension is based on voluntary contributions and ORSO is so much smaller in dollar value compared to the very substantial mandatory MPF/CPF dollar value pot of Hong Kong.

Due to the slow economies in Hong Kong and China, stagnant equity markets, real estate meltdown, and competitive pressure from Hong Kong-based pension and wealth management platforms, we do not expect any significant/meaningful contribution to IFAST’s AUA figures from Hong Kong ORSO pot.

Intense competition and iFast’s outdated/lagging services (e.g., FSMone apps) mean that the small, mature market in Singapore still accounts for the vast majority of IFAST’s AUA (~70%) since 2000.

iFast FSMone can’t compete for brokerage assets with numerous much faster and more tech-savvy competitors such as MooMoo, Tiger, Endowus, IBKR, Saxo, POEMS, WeBull, Syfe, CMC, LongBridge, uSmart, and so many more.

4. “At its latest earnings briefing, iFast chief executive Lim Chung Chun said revenue recognition for the ePension division will increase as overall onboarding level goes up.”

[Sakura Research]: We agree with this assessment and do not dispute it. The onboarding of Trustees will conclude in 2025.

Our main concern is the potential drop in HK ePension revenues and profits in 2026.

Here, we anticipate a precipitous revenues decline of 70%-80% starting in 2026.

Can iFast provide revenue or profit guidance from 2026 Hong Kong operations?

5. “However, UOB Kay Hian (UOBKH) analyst Heidi Mo said these banks may not be a fair comparison.

Instead, she noted that the company is focused on both transaction banking and personal banking, where the customer base is larger and revenue from loans is generated. She added that iFast Global Bank’s net interest margin stands at about 1 per cent.”

[Sakura Research]: iFast Bank iGB does not extend retail or business loans, which limits its ability to earn higher yields and make a meaningful contribution to profits and return on equity (ROE). The Bank takes depositors’ money and invests it in low-yield, low-risk bonds.

According to iFast Bank Ltd’s annual report for 2023, net interest income (NII) was £1,701,000, up from £121,000 in 2022. With lowering interest rates in the UK and EU, the bank will face a more challenging financial environment in which to grow its NII.

Net fee and commission income (from remittances, i.e. EzRemit) was £3,557,000, compared to £3,656,000 in 2022, representing a drop of approximately 3%. Despite having more customers in 2023, the Bank recorded less operating income from its main business, Remittances. Again, this highlights the intense competition in the remittance sector from both traditional players and advanced fintech competitors.

We believe iFast Bank is essentially a glorified remittance service provider, competing against numerous traditional players as well as fintech giants such as Revolut, Wise, Nium, YouTrip, Western Union, PayPal, XE, and others.

We expect iGB Bank to continue burning cash, incurring losses, and requiring additional cash infusions in 2025 and 2026. This is why iFast recently raised S$100 million in bonds at 4.3% in June and used a substantial portion of these bond proceeds to inject GBP 14.99 million into iGB Bank.

6. “As for iFast’s profitability and cash flows, Sakura Research said the company has experienced a fall in operating profit as a ratio to AUA. In the company’s 2023 annual report, this figure fell from 0.209 per cent in 2021 to 0.047 per cent in 2023.

However, UOBKH’s Mo noted that the company’s profit before tax for the latest half year stood at S$37.9 million, while AUA stood at S$22.37 billion. This brings the ratio back up to 0.169 per cent, which is higher than the 0.081 per cent in 2022.”

[Sakura Research]: Hong Kong ePension profits do not stem from platform AUA or wealth management. Instead, ePension profits come primarily from providing back-end and front-end IT services to PCCW / eMPF, with a significant portion of this work done by iFast’s Malaysia IT ‘sweatshop’.

The operating profit % margins of wealth management/fintech per AUA are dropping to record lows due to intense competition in every iFast market since the peak of the COVID-19 pandemic.

In summary, ePension profits are not based on AUA. Don’t count ePension profits as part of Core platform operating profits per AUA. Unfortunately, Ms. Heidi Mo does not seem to realize this.

In conclusion, we hope that IFAST management will agree to respond to Sakura Research Accounting questions and allegations.

We believe that there are critical cash flow, balance sheet, and accounting questions and issues that must be addressed for the benefit of the investing public and all stakeholders.

https://www.scribd.com/document/763110745/Accounting-Questions-for-IFAST-Corporation-Ltd

https://sakuraresearch.com/?p=22

We also hope to receive comments from other research analysts (including from DBS, UBS, CGSI, and Citi).

By viewing and/or using material on this website you agree to the Terms.

Use of Sakura Research materials is at your own risk.

THIS RESEARCH EXPRESSES SOLELY OUR OPINIONS.